Social Security Changes 2026: Key Updates & Financial Impact

Advertisers

Understanding the upcoming Social Security Changes 2026 is crucial for beneficiaries to navigate potential adjustments in benefits, ensure financial stability, and effectively plan for their future.

The landscape of retirement planning and financial security is constantly evolving, and for millions of Americans, Social Security remains a cornerstone of that stability. As we look ahead to 2026, significant discussions and potential legislative actions are on the horizon that could reshape the program. Understanding these Social Security Changes 2026 is not just for future retirees; it’s essential for current beneficiaries and anyone planning their financial future to grasp the potential impacts and prepare accordingly. This article aims to cut through the complexity and provide clear, actionable insights into what these adjustments might entail.

Advertisers

Understanding the Current State of Social Security

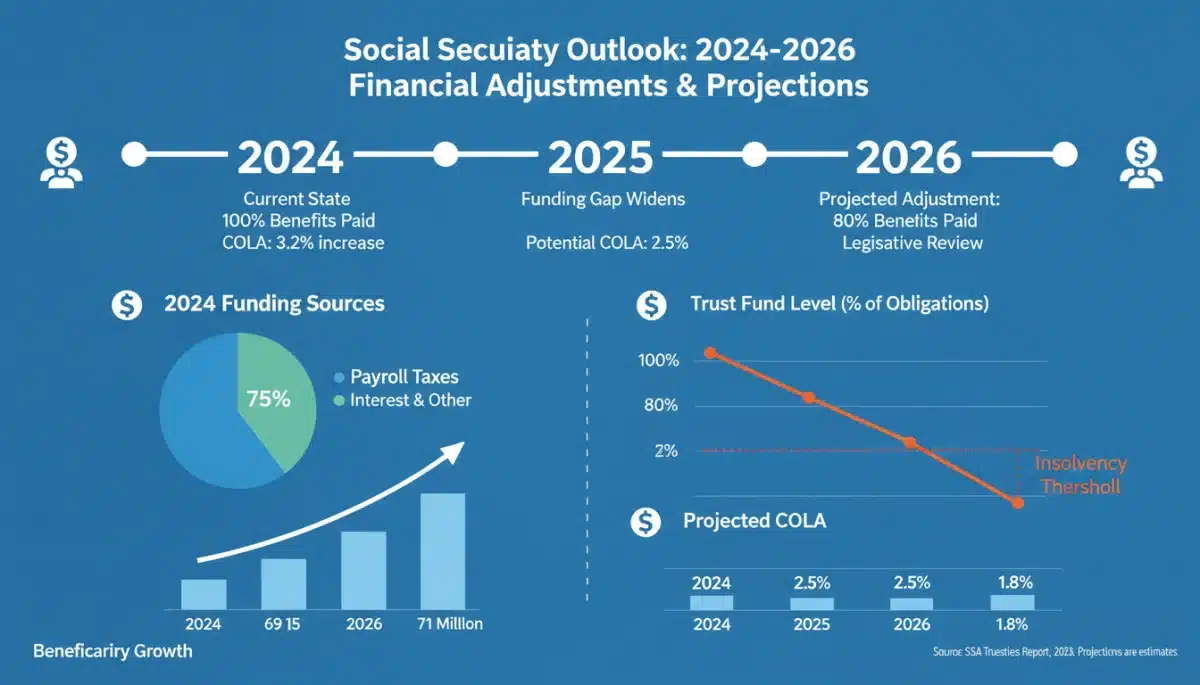

Before delving into future adjustments, it’s crucial to understand the current health and operational framework of Social Security. The program, established in 1935, primarily functions as a pay-as-you-go system, where current workers’ contributions fund the benefits of today’s retirees and other beneficiaries. This foundational structure has served generations, but demographic shifts and economic pressures are continually testing its long-term solvency.

The Social Security Administration (SSA) regularly releases trustee reports that project the financial outlook of the program. These reports are vital for understanding the challenges and potential solutions. For instance, recent reports have highlighted that while the Old-Age and Survivors Insurance (OASI) Trust Fund currently has sufficient assets to pay benefits for several years, it faces projected shortfalls in the long run if no legislative action is taken. This isn’t a new concern, but the urgency for reform intensifies with each passing year, making the prospect of Social Security Changes 2026 a significant topic.

Advertisers

Key Components of Social Security Funding

- Payroll Taxes: The primary source of funding, collected from workers and employers.

- Taxation of Benefits: A portion of Social Security benefits can be subject to federal income tax for some recipients.

- Interest on Trust Fund Investments: Funds not immediately needed are invested in special U.S. Treasury securities, earning interest.

The balance between incoming contributions and outgoing benefits is delicate. When the number of retirees grows faster than the number of contributing workers, or when economic conditions lead to slower wage growth, the system experiences pressure. This pressure is what drives the need for potential adjustments, ensuring the program can continue to fulfill its promises to future generations. Understanding these fundamentals helps contextualize why changes are being discussed and why they are so critical for the program’s sustainability.

Projected Demographic Shifts and Their Impact

One of the most significant drivers behind the anticipated Social Security Changes 2026 is the evolving demographic landscape of the United States. The nation is experiencing a profound shift, characterized by an aging population and declining birth rates. These trends have a direct and substantial impact on the Social Security system, which relies on a healthy ratio of workers to beneficiaries.

The baby boomer generation, a large cohort born between 1946 and 1964, has been entering retirement in increasing numbers over the past decade. This demographic wave means more people are drawing benefits, while the subsequent generations, though still contributing, are not as numerically large. Consequently, the worker-to-beneficiary ratio is decreasing. In simpler terms, fewer working individuals are contributing per retiree, placing a greater strain on the trust funds.

Understanding the Worker-to-Beneficiary Ratio

- Historical Context: In 1950, there were 16.5 workers for each Social Security beneficiary.

- Current Ratio: This ratio has significantly declined to roughly 2.7 workers per beneficiary.

- Projected Future: By 2035, projections suggest it could drop further to 2.3 workers per beneficiary.

This imbalance is not merely an academic concern; it has tangible implications for the program’s solvency. Without adjustments, the trust funds are projected to be depleted, meaning Social Security would only be able to pay out a portion of promised benefits. This stark reality underscores the urgency for policymakers to address these demographic challenges, making discussions around Social Security Changes 2026 particularly relevant and critical for the financial well-being of millions.

Potential Legislative Adjustments on the Horizon

As the need for reform becomes more pressing, various legislative proposals are being discussed to ensure the long-term solvency of Social Security. These proposals often fall into broad categories: increasing revenue, decreasing expenditures, or a combination of both. While no specific plan has been finalized for Social Security Changes 2026, understanding the types of adjustments being considered can help beneficiaries anticipate potential impacts.

One common approach to increasing revenue is to raise the Social Security payroll tax rate. This would mean workers and employers contribute a slightly higher percentage of their earnings to the program. Another strategy involves increasing the earnings cap, which is the maximum amount of earnings subject to Social Security taxes. Currently, earnings above this cap are not taxed for Social Security purposes. Raising or eliminating this cap would bring more income into the system, predominantly from higher earners.

On the expenditure side, proposals often include adjusting the full retirement age (FRA), which is the age at which individuals can claim 100% of their earned benefits. Raising the FRA would mean individuals would either have to work longer or accept reduced benefits if they claim earlier. Other discussions involve changing the Cost-of-Living Adjustment (COLA) formula, which determines annual benefit increases. Modifying this formula could result in smaller annual increases for beneficiaries.

Commonly Discussed Legislative Options

- Increase Payroll Tax Rate: A small percentage increase for workers and employers.

- Raise Earnings Cap: Subject more of high earners’ income to Social Security taxes.

- Adjust Full Retirement Age: Gradually increase the age at which full benefits are received.

- Modify COLA Formula: Implement a different index for calculating annual benefit increases.

Each of these potential adjustments carries its own set of implications, affecting different beneficiary groups in various ways. The debate surrounding these changes is complex, balancing the need for solvency with the impact on individuals’ financial security. As 2026 approaches, these discussions will intensify, and beneficiaries should stay informed about the evolving legislative landscape.

Financial Impact on Current and Future Beneficiaries

The prospect of Social Security Changes 2026 naturally raises concerns among both current and future beneficiaries regarding their financial well-being. The specific impact will, of course, depend on the nature of the reforms enacted. However, it’s possible to outline general scenarios based on the types of adjustments most frequently discussed.

For current retirees, changes to the COLA formula could be the most immediate and noticeable. A modified COLA could mean smaller annual increases, leading to a gradual erosion of purchasing power over time, especially in periods of high inflation. While a drastic cut to current benefits is generally considered politically unfeasible, any reduction in the rate of increase can still have a significant cumulative effect on fixed incomes.

Impact Scenarios for Beneficiaries

- Current Retirees: Potentially smaller annual benefit increases due to COLA adjustments.

- Near-Retirees (within 5-10 years): Could face a higher full retirement age, requiring them to work longer or accept reduced benefits.

- Younger Workers: May see a combination of higher payroll taxes, increased full retirement age, and potentially altered benefit formulas in the long run.

Future beneficiaries, particularly younger generations, might experience a more comprehensive set of changes. A higher full retirement age would necessitate longer careers or a re-evaluation of retirement timelines. Increased payroll taxes would reduce take-home pay, and any adjustments to benefit calculation formulas could alter expected retirement income. It’s important for everyone to monitor these discussions and consider how potential Social Security Changes 2026 might influence their personal financial planning and savings strategies. Proactive planning is key to mitigating any adverse effects.

Strategies for Adapting to Future Changes

Given the potential for Social Security Changes 2026, adopting proactive strategies is crucial for individuals at every stage of their financial journey. Waiting for legislation to be finalized before planning could leave many unprepared. Instead, a flexible and informed approach can help mitigate risks and ensure continued financial stability.

For those nearing retirement, it’s advisable to re-evaluate your retirement timeline and income projections. If the full retirement age is raised, you might consider working a few extra years to maximize your benefits or adjust your claiming strategy. Diversifying retirement income sources beyond Social Security is also paramount. Relying solely on Social Security has always carried risks, and potential changes only underscore the importance of a robust personal savings and investment plan.

Key Adaptation Strategies

- Review Retirement Projections: Reassess your expected income and expenses in retirement.

- Diversify Income Streams: Build up personal savings, investments, and other retirement accounts.

- Consider Working Longer: If physically able, extending your career can increase benefits and reduce the period you rely on savings.

- Stay Informed: Continuously monitor legislative developments and expert analyses regarding Social Security.

Younger workers have the advantage of time, which is a powerful asset in financial planning. Starting to save and invest early, even small amounts, can accumulate substantial wealth over decades. Understanding the potential for higher payroll taxes or a later full retirement age can motivate earlier and more aggressive contributions to 401(k)s, IRAs, and other personal savings vehicles. By taking these steps, individuals can build a stronger financial foundation, making them less dependent on the unpredictable nature of future Social Security reforms and better prepared for any Social Security Changes 2026 and beyond.

The Role of Advocacy and Public Engagement

The future of Social Security is not solely determined by politicians and actuaries; public engagement and advocacy play a significant role in shaping policy decisions. As discussions around Social Security Changes 2026 intensify, beneficiaries and concerned citizens have opportunities to voice their perspectives and influence the outcome. Understanding how to engage effectively can make a difference in protecting the program’s integrity and ensuring equitable adjustments.

Advocacy groups, often representing retirees, workers, and specific demographic segments, actively lobby lawmakers and raise public awareness about proposed changes. These organizations provide valuable information and a platform for collective action. Supporting such groups or participating in their campaigns can amplify individual voices and bring diverse concerns to the forefront of the legislative debate. Public forums, town halls, and online petitions are also avenues for expressing opinions directly to elected officials.

Ways to Engage and Advocate

- Contact Elected Officials: Share your concerns and opinions with your representatives.

- Support Advocacy Groups: Join or donate to organizations championing Social Security’s future.

- Participate in Public Discussions: Attend town halls or online forums to voice your perspective.

- Educate Yourself and Others: Stay informed about proposed changes and share accurate information.

In a democratic society, informed public discourse is essential for crafting sound policy. By staying educated on the complexities of Social Security, understanding the various reform proposals, and actively participating in the conversation, individuals can help ensure that any Social Security Changes 2026 are thoughtful, balanced, and serve the best interests of all Americans. This collective effort is vital for preserving a program that has provided a safety net for millions for nearly a century.

| Key Point | Brief Description |

|---|---|

| Demographic Shifts | An aging population and fewer workers per beneficiary are straining the system, necessitating reform. |

| Legislative Proposals | Options include increasing payroll taxes, raising the earnings cap, or adjusting the full retirement age. |

| Beneficiary Impact | Potential changes could affect annual benefit increases, retirement age, and overall retirement income. |

| Adaptation Strategies | Reviewing retirement plans, diversifying income, and staying informed are crucial for financial resilience. |

Frequently Asked Questions About Social Security Changes 2026

The main drivers are demographic shifts, particularly the aging population and lower birth rates, which are reducing the ratio of workers contributing to beneficiaries receiving payments, straining the system’s finances.

While direct cuts to current benefits are less likely, changes to the Cost-of-Living Adjustment (COLA) formula could result in smaller annual increases, affecting your purchasing power over time. Final decisions are pending legislative action.

Legislative proposals often include gradually increasing the full retirement age. This would mean future retirees might need to work longer to receive their full benefits or accept reduced benefits if they claim earlier.

It’s advisable to review your retirement plan, diversify your income sources beyond Social Security, consider working longer if feasible, and stay informed about policy developments. Proactive financial planning is key.

The official Social Security Administration (SSA) website, particularly their annual trustee reports, offers the most authoritative information. Reputable financial news outlets and non-partisan advocacy groups also provide valuable insights and analyses.

Conclusion

The anticipated Social Security Changes 2026 represent a critical juncture for a program that has long served as a bedrock of American retirement security. While the exact nature of these adjustments remains subject to ongoing legislative debate, understanding the underlying demographic and financial pressures is paramount. Current and future beneficiaries must remain vigilant, proactive, and informed to navigate these potential shifts effectively. By engaging in personal financial planning, diversifying income streams, and staying abreast of policy discussions, individuals can better prepare for any eventual reforms, ensuring their long-term financial stability in a changing economic landscape.