US Real Estate 2026: 5% Appreciation Still Achievable?

Advertisers

Forecasting US real estate market trends for 2026, a 5% appreciation for homeowners remains a plausible, though not guaranteed, scenario, heavily influenced by inflation, interest rates, and localized supply-demand dynamics.

Advertisers

The question on many homeowners’ minds as we approach the middle of the decade is whether the robust growth seen in previous years can be sustained. Specifically, homeowners are keenly watching the US real estate 2026 market, wondering if a 5% appreciation is still a realistic expectation. This article delves into the various factors shaping the housing landscape, providing insights into what 2026 might hold for property values across the United States.

Understanding the Current Real Estate Climate

To project where the market might be in 2026, it’s crucial to first understand the forces currently at play. The past few years have been characterized by unprecedented shifts, from record-low interest rates fueling a buying frenzy to subsequent rate hikes tempering demand. These fluctuations have created a complex environment, making accurate forecasts a challenging but essential endeavor for homeowners and prospective buyers alike.

Advertisers

Several key economic indicators are constantly being monitored by analysts. Inflation, employment rates, and consumer confidence all contribute to the overall health of the housing sector. A robust job market, for instance, typically translates into more potential buyers, while high inflation can erode purchasing power, even if wages are increasing. The interplay of these forces dictates market momentum.

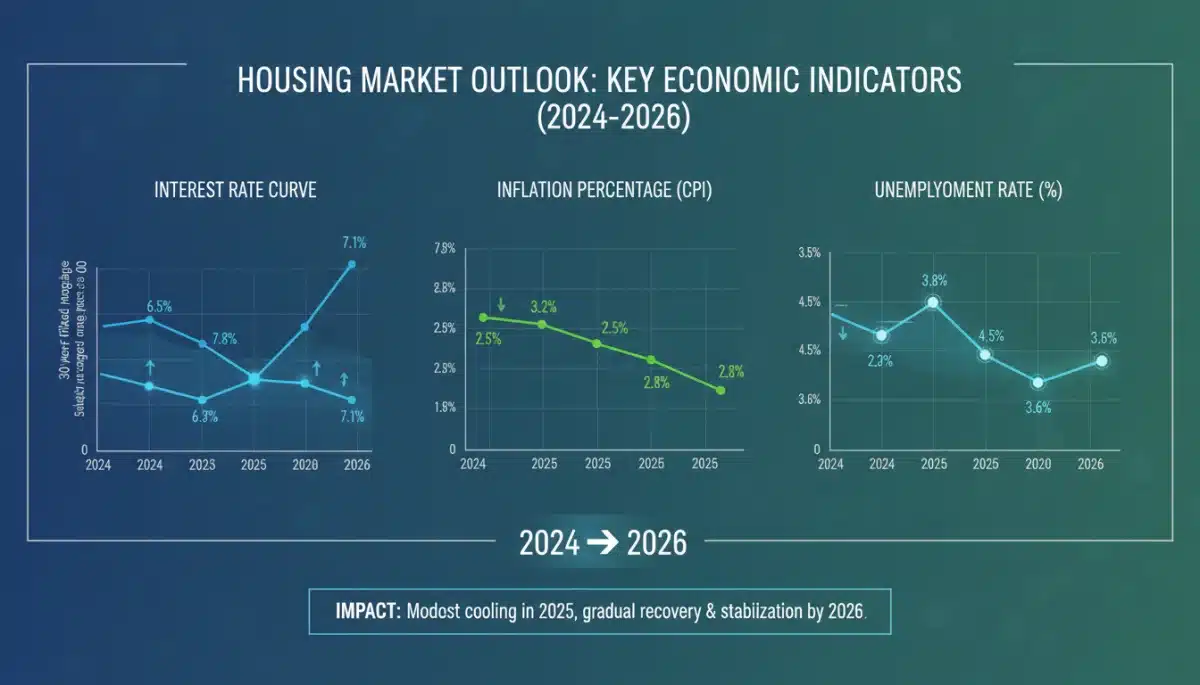

The Impact of Interest Rates on Affordability

Interest rates are arguably the most significant external factor influencing housing affordability and, consequently, home prices. When rates are low, borrowing becomes cheaper, enabling more buyers to enter the market and push prices upward. Conversely, higher rates can cool demand significantly.

- Mortgage Rate Volatility: Recent years have shown how quickly mortgage rates can change, directly impacting monthly payments.

- Buyer Behavior: Higher rates often lead to a reduction in buyer activity, as purchasing power diminishes.

- Refinancing Trends: Existing homeowners might be less inclined to sell if they hold onto historically low mortgage rates.

The Federal Reserve’s monetary policy, driven by inflation targets and economic stability goals, will continue to be a primary determinant of these rates. Any indication of sustained inflation or economic slowdown could prompt further adjustments, reverberating through the housing market.

Understanding the current real estate climate requires a nuanced view of both national economic policies and localized market conditions. While broad trends provide a framework, the specifics of a particular region or city can often diverge, highlighting the importance of granular analysis for homeowners.

Economic Projections for 2026 and Housing Demand

Looking ahead to 2026, economic projections paint a picture of continued evolution. While a recession has been a persistent concern, many economists anticipate a period of slower but stable growth. This economic backdrop will inevitably shape housing demand, influencing both the number of potential buyers and their financial capacity.

Demographic shifts also play a substantial role. Millennials and Gen Z are increasingly entering prime homebuying ages, representing a significant cohort of potential demand. Their preferences, financial situations, and preferred living arrangements will dictate where and what kind of housing is most sought after. This generational wave could provide a consistent floor for demand, even in the face of other economic headwinds.

Population Growth and Urbanization Trends

The movement of people within the United States continues to influence housing dynamics. Certain states and cities are experiencing rapid population growth, driven by job opportunities and lifestyle preferences.

- Sun Belt Migration: Southern and Southwestern states continue to attract residents, boosting housing demand in these regions.

- Remote Work Impact: The flexibility of remote work has allowed some to move away from expensive urban centers, impacting demand in suburban and rural areas.

- Urban Core Revitalization: While some have left, many urban centers are also seeing renewed interest, particularly among younger demographics.

These migratory patterns create localized pressure points, where demand can far outstrip supply, leading to accelerated price appreciation. Conversely, areas experiencing population stagnation or decline may see more muted growth or even depreciation.

Overall, the economic projections for 2026 suggest a market that will likely be more balanced than the frenetic pace of the early 2020s but still underpinned by steady demand from a growing and shifting population base. The ability to achieve 5% appreciation will depend heavily on how these broad trends manifest at the local level.

Supply-Side Dynamics: Inventory and Construction

The supply of available housing remains a critical factor in determining price appreciation. For years, the US housing market has grappled with an inventory shortage, a legacy of underbuilding following the 2008 financial crisis. This persistent imbalance between supply and demand has been a primary driver of home price increases.

As we approach 2026, the pace of new construction will be under scrutiny. Builders face various challenges, including rising material costs, labor shortages, and regulatory hurdles, all of which can impede their ability to bring new homes to market efficiently. However, sustained demand and attractive profit margins could incentivize increased construction activity.

Challenges and Opportunities in New Home Construction

Building new homes is a complex undertaking, fraught with economic and logistical difficulties that directly influence the available housing stock.

- Material Costs: Fluctuations in the cost of lumber, concrete, and other essential building materials impact construction budgets.

- Labor Shortages: A persistent shortage of skilled construction workers can delay projects and increase labor costs.

- Zoning and Regulations: Local zoning laws and lengthy permitting processes can slow down the development of new housing units.

Despite these challenges, innovations in construction, such as modular homes and improved efficiencies, offer opportunities to boost supply. Furthermore, government incentives and streamlined regulatory processes could also play a role in accelerating new home builds.

The supply-side dynamics for 2026 will largely dictate whether the market remains tight or begins to find a healthier equilibrium. A significant increase in inventory, particularly of starter homes, could temper price growth, making a 5% appreciation more challenging to achieve across the board. Conversely, continued low inventory would likely sustain upward pressure on prices.

Regional Variations and Local Market Nuances

While national trends provide a broad overview, the US real estate market is fundamentally a collection of local markets. What happens in, say, Boise, Idaho, can be vastly different from the trends observed in Miami, Florida, or Austin, Texas. These regional variations are crucial for homeowners assessing their potential for appreciation.

Factors such as local job growth, industry diversification, population influx, and even specific city ordinances can create microclimates within the broader housing market. A city with a booming tech sector, for instance, might see sustained demand and higher appreciation rates, even if national growth is moderate.

Key Factors Driving Local Market Performance

Understanding the specific drivers within a local market is paramount for predicting its future trajectory.

- Job Market Strength: Areas with robust job creation and diverse industries tend to attract more residents and support higher home values.

- Affordability: Relative affordability compared to income can influence migration patterns and sustained demand.

- Quality of Life: Access to amenities, good schools, and recreational opportunities can make a region highly desirable, driving up prices.

Homeowners should research local economic forecasts, population growth projections, and planned infrastructure developments in their specific area. These localized insights will offer a more accurate picture of potential appreciation than national averages alone.

Therefore, while a 5% appreciation might be achievable in some high-demand, growth-oriented markets, it might be an ambitious target in others. The key lies in understanding the unique characteristics and economic forces shaping one’s specific locale.

Inflation, Property Taxes, and Homeowner Costs

Beyond the headline appreciation rate, homeowners must also consider the broader economic context, particularly inflation and its impact on property-related costs. While a 5% increase in home value sounds appealing, its real value can be eroded if inflation is equally high or higher. The purchasing power of that appreciation becomes a crucial consideration.

Property taxes, insurance premiums, and maintenance costs are all subject to inflationary pressures. These ongoing expenses can significantly offset the financial benefits of home appreciation, impacting a homeowner’s overall equity and net wealth. Understanding these expenditures is vital for a holistic view of homeownership in 2026.

Rising Operational Costs for Homeowners

The cost of owning a home extends far beyond the mortgage payment and initial purchase price. These ongoing expenses are critical to evaluate.

- Property Tax Adjustments: As home values rise, so too can property taxes, especially in areas with frequent reassessments.

- Insurance Premiums: Climate-related risks and rising repair costs are driving up homeowner insurance premiums across many regions.

- Maintenance and Utilities: The cost of home repairs, utilities, and general upkeep can increase significantly with inflation.

These rising operational costs mean that even with a healthy appreciation, the net financial gain for homeowners might be less pronounced than the raw percentage suggests. Strategic budgeting and proactive maintenance become even more important in an inflationary environment.

Ultimately, achieving a meaningful 5% appreciation in 2026 requires not just an increase in market value, but also a careful management of the escalating costs associated with homeownership. Homeowners should factor these expenses into their financial planning to truly understand the benefits of their property’s growth.

Is a 5% Appreciation Still Achievable for Homeowners?

The central question for many homeowners is whether a 5% appreciation in their property value by 2026 is a realistic goal. Based on current economic trajectories, demographic trends, and supply-demand dynamics, a 5% appreciation appears to be an achievable, though not guaranteed, outcome in many parts of the US real estate market.

However, it is crucial to recognize that this will not be a uniform experience. Some markets, particularly those experiencing strong job growth, limited new construction, and sustained population influx, are more likely to see such appreciation. Conversely, areas with declining populations, oversupply, or economic stagnation may experience slower growth or even modest depreciation.

Factors Influencing Future Appreciation Potential

Several key elements will collectively determine the likelihood of achieving a 5% appreciation.

- Interest Rate Stability: A more stable interest rate environment would reduce market volatility and support consistent buyer demand.

- Inflationary Control: Successful efforts to manage inflation would bolster purchasing power and the real value of appreciation.

- Balanced Inventory: A gradual increase in housing supply without overwhelming demand would lead to more sustainable growth.

- Economic Resilience: Strong, diversified local economies will be better positioned to weather any national economic headwinds.

For homeowners, proactive engagement with local market data, understanding economic forecasts, and maintaining their property will be key strategies. While national averages provide a benchmark, the story of US real estate 2026 appreciation will ultimately be told at the neighborhood level.

In conclusion, while a 5% appreciation is a plausible target for many homeowners by 2026, it requires a careful consideration of both macro-economic factors and highly localized market conditions. The dream of consistent home value growth remains alive, but it demands informed decision-making and a realistic outlook.

| Key Point | Brief Description |

|---|---|

| Interest Rate Influence | Mortgage rates significantly impact affordability and buyer demand, influencing home price trajectories. |

| Supply-Demand Balance | Inventory shortages continue to drive prices, with new construction facing various challenges. |

| Regional Market Variation | Appreciation rates vary greatly by local job growth, population shifts, and economic health. |

| Inflationary Impact | Rising property taxes, insurance, and maintenance costs can offset nominal appreciation gains. |

Frequently Asked Questions About 2026 US Real Estate

While precise predictions are challenging, many economists anticipate a period of relative stability or slight moderation in interest rates by 2026, assuming inflation remains under control. Significant hikes are less likely unless unforeseen economic shocks occur.

Regions with strong job markets, growing populations, and limited housing supply, such as parts of the Sun Belt (e.g., Florida, Texas, Arizona) and select tech hubs, are generally forecast to experience higher appreciation rates.

Remote work will likely continue to decentralize demand, boosting values in suburban and exurban areas previously considered less desirable. It may also sustain demand in smaller cities with good amenities and lower costs of living.

While construction has increased, it generally still lags behind the demand fueled by demographic growth and household formation. Supply chain issues and labor shortages continue to be hurdles, maintaining upward price pressure in many areas.

To maximize appreciation, homeowners should focus on property maintenance, strategic renovations, and staying informed about local market trends. Understanding economic shifts and demographic changes in their area is also crucial.

Conclusion

The prospect of a 5% appreciation in the US real estate market by 2026 is a complex one, influenced by a confluence of economic, demographic, and supply-side factors. While national averages may paint a broad picture, the reality will be highly localized, with some markets outperforming and others experiencing more moderate growth. Homeowners should remain vigilant, monitoring interest rate movements, inflation trends, and, most importantly, the specific dynamics of their local housing market. Informed decision-making, coupled with a focus on property value and managing associated costs, will be paramount in navigating the evolving landscape of US real estate 2026 and securing a favorable return on their investment.