Medicare Part D in 2026: Your Guide to Best Prescription Drug Coverage

Advertisers

Understanding Medicare Part D in 2026 is crucial for securing affordable prescription drug coverage, requiring careful comparison of plans to align with individual health and financial situations.

Navigating Medicare Part D in 2026: Comparing Plans and Finding the Best Prescription Drug Coverage for You can feel overwhelming, but securing the right plan is vital for your health and financial well-being. This guide will demystify the complexities, helping you make informed decisions about your prescription drug coverage.

Advertisers

Understanding Medicare Part D: The Basics for 2026

Medicare Part D is the component of Medicare that provides prescription drug coverage. It was established to help beneficiaries manage the costs of their medications, which can be substantial. In 2026, Part D continues its role as a crucial safety net, though its structure and available plans might see adjustments based on legislative changes and market dynamics. Understanding the core principles of Part D is the first step toward effective plan selection.

Part D plans are offered by private insurance companies approved by Medicare. These plans vary widely in terms of premiums, deductibles, formularies (lists of covered drugs), and cost-sharing structures. It’s not a one-size-fits-all solution; what works for one person might not be ideal for another. The annual enrollment period is your opportunity to review and change your plan, ensuring it still meets your needs.

Advertisers

What’s New or Reinforced in 2026?

While specific legislative changes for 2026 are still being finalized, general trends point towards continued efforts to lower out-of-pocket costs for beneficiaries. This includes potential caps on annual drug spending and adjustments to the coverage gap, often referred to as the ‘donut hole’. Staying informed about these changes is paramount.

- Lower Out-of-Pocket Caps: Anticipate further reductions in the maximum amount you’ll pay for prescription drugs annually.

- Formulary Transparency: Increased focus on making drug lists clearer and easier to understand.

- Insulin Cost Controls: Continued efforts to cap insulin costs for many beneficiaries.

In essence, Medicare Part D in 2026 aims to provide more predictable and affordable prescription drug coverage. Familiarizing yourself with these foundational elements will empower you to compare plans more effectively and choose the best option for your unique circumstances.

Decoding Part D Costs: Premiums, Deductibles, and Co-pays

The financial structure of Medicare Part D can be intricate, involving several layers of costs that beneficiaries need to understand. These costs significantly influence the overall affordability and value of a plan. The three primary cost components are premiums, deductibles, and co-payments/coinsurance.

A plan’s premium is the monthly fee you pay to the insurance company for your coverage. This amount can vary significantly between plans and is separate from your Medicare Part B premium. Some plans might have a $0 premium, but these often come with higher deductibles or co-pays for certain drugs. Your income level can also affect your premium through the Income-Related Monthly Adjustment Amount (IRMAA).

Understanding Deductibles and Co-payments

The deductible is the amount you must pay out-of-pocket for your prescriptions before your plan starts to pay. For 2026, this amount will likely be adjusted from previous years, so it’s critical to check the specific deductible for each plan you consider. After meeting your deductible, you typically pay a co-payment (a fixed amount) or coinsurance (a percentage of the drug cost) for your medications.

- Premium: Monthly fee for the plan, varying by provider and potentially by income.

- Deductible: Annual amount you pay before coverage kicks in.

- Co-pays/Coinsurance: Your share of the cost for each prescription after the deductible.

It’s important to analyze how these costs interact with your specific prescription needs. A plan with a low premium might have a high deductible, making it less suitable if you have expensive medications early in the year. Conversely, a higher premium might offer a lower deductible or even no deductible, potentially saving you money if you have regular, costly prescriptions. Careful evaluation of your anticipated drug costs against these plan structures is key to finding the most economical option.

Navigating the Formulary: Your Drug List Explained

The formulary is perhaps one of the most critical aspects of any Medicare Part D plan. It’s the list of prescription drugs covered by the plan. Each plan’s formulary is different, and understanding how it works is essential for ensuring your specific medications are covered and at what cost. Plans typically organize drugs into tiers, with each tier having a different co-payment or coinsurance amount.

Generally, generic drugs are on lower tiers with the lowest co-pays, while brand-name drugs and specialty medications are on higher tiers with higher costs. It’s imperative not just to check if your drugs are on the formulary, but also to see which tier they fall into. A drug might be covered, but if it’s on a high tier, your out-of-pocket cost could still be substantial.

Formulary Changes and Exceptions

Formularies can change throughout the year, though plans must notify you if a drug you’re taking is removed or moved to a higher cost-sharing tier. If your drug isn’t on a plan’s formulary, or if you believe it’s in the wrong tier, you have the right to request a formulary exception. This process involves your doctor providing medical justification for the specific drug.

- Tiered System: Drugs categorized into tiers, affecting co-pay amounts.

- Generic vs. Brand: Generics usually in lower, more affordable tiers.

- Exception Process: Option to request coverage for non-formulary drugs or re-tiering.

When comparing plans for Medicare Part D in 2026, always start by checking if all your current medications are on the formulary. If you anticipate needing new medications, consider plans with broad coverage. Don’t hesitate to contact the plan directly or use Medicare’s plan finder tool to verify coverage and costs for your specific prescriptions. This proactive approach can prevent unexpected expenses.

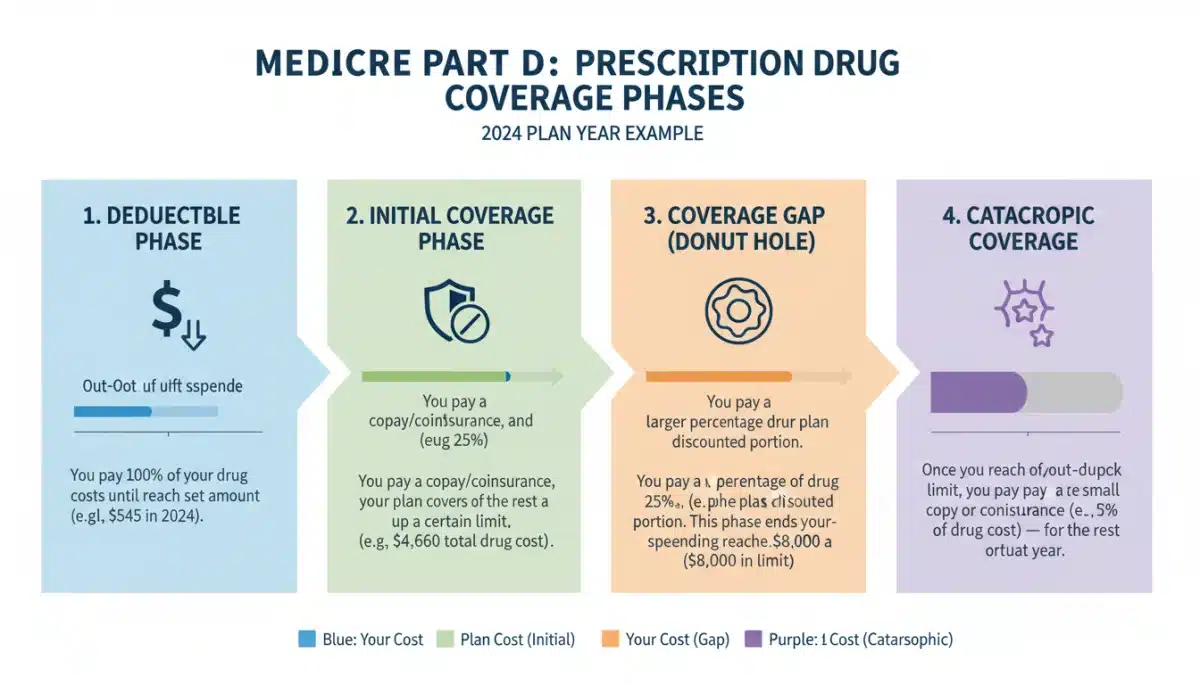

The Coverage Gap (Donut Hole) and Catastrophic Coverage in 2026

The Medicare Part D coverage structure includes several phases, two of the most significant being the coverage gap, commonly known as the ‘donut hole’, and catastrophic coverage. While reforms have significantly reduced the impact of the donut hole, it’s still an important concept to understand when evaluating plans for 2026.

The coverage gap begins after you and your plan have together spent a certain amount on covered drugs. In this phase, you typically pay a higher percentage of the drug cost. However, due to the Affordable Care Act and subsequent legislation, your out-of-pocket costs in the donut hole are now limited to 25% for both generic and brand-name drugs. This means you pay 25% of the cost, and the plan and drug manufacturers cover the rest.

Reaching Catastrophic Coverage

Once your out-of-pocket spending reaches a certain threshold (which includes your deductible, co-pays, and what you pay in the coverage gap), you enter the catastrophic coverage phase. In this phase, your costs for covered drugs become very low, typically a small co-payment or coinsurance for the remainder of the year. For 2026, there are further improvements, including a new $2,000 annual cap on out-of-pocket drug costs for all Medicare Part D beneficiaries, significantly enhancing financial protection.

- Coverage Gap (Donut Hole): You pay 25% of drug costs for both generics and brands.

- Catastrophic Coverage: Starts after reaching annual out-of-pocket maximum, with minimal costs.

- 2026 Out-of-Pocket Cap: A new $2,000 annual limit on drug spending for all beneficiaries.

Understanding these phases is crucial, especially if you have high prescription drug costs. The new $2,000 out-of-pocket cap for 2026 is a game-changer, offering substantial financial relief and predictability. When comparing plans, consider how quickly you might reach these thresholds based on your current medication regimen and the plan’s specific cost-sharing structure.

Comparing Part D Plans: Tools and Strategies for 2026

With numerous Medicare Part D plans available, comparing them effectively is essential to finding the best fit. The key is to use the right tools and adopt a strategic approach. Medicare’s official website offers a powerful Plan Finder tool that is indispensable for this process. This tool allows you to enter your specific medications and dosages, then compares plans based on your estimated annual out-of-pocket costs.

Beyond the Plan Finder, consider consulting with independent insurance agents or organizations like the State Health Insurance Assistance Program (SHIP). These resources can provide personalized guidance and help you navigate the complexities of plan selection without bias. They can also help clarify any questions you might have about specific plan benefits or restrictions.

Key Comparison Strategies

When comparing plans, look beyond just the monthly premium. A low premium might hide high deductibles or co-pays for your specific drugs. Conversely, a slightly higher premium might offer better overall value if it significantly reduces your out-of-pocket costs throughout the year. Always create a comprehensive list of your medications, including dosages and frequency, before you begin your comparison.

- Utilize Medicare Plan Finder: Enter your drugs for personalized cost estimates.

- Consult Experts: Seek advice from SHIP or independent insurance agents.

- Total Annual Cost: Focus on the estimated total cost, not just the premium.

The goal is to find a plan that minimizes your total annual spending on prescription drugs, considering premiums, deductibles, and co-payments. Pay close attention to a plan’s formulary and how your drugs are tiered. By diligently using the available tools and strategies, you can confidently choose the optimal Medicare Part D in 2026 plan that aligns with your health needs and budget.

Enrollment Periods and How to Enroll in Part D for 2026

Understanding the various enrollment periods for Medicare Part D is crucial to ensure you get the coverage you need when you need it. Missing an enrollment deadline can result in delays in coverage or even late enrollment penalties, which can increase your premiums permanently.

The primary enrollment period for most people is when they first become eligible for Medicare, typically around their 65th birthday. This is called the Initial Enrollment Period (IEP). It lasts for seven months, beginning three months before your 65th birthday month, includes your birthday month, and extends three months after. If you don’t sign up for Part D when you’re first eligible and don’t have other creditable drug coverage, you might face a late enrollment penalty.

Annual Enrollment and Special Enrollment Periods

The Annual Enrollment Period (AEP), also known as Open Enrollment, runs from October 15 to December 7 each year. During this time, you can join, switch, or drop a Medicare Part D plan, with new coverage starting on January 1 of the following year. This is your opportunity to re-evaluate your current plan and compare it against other options for Medicare Part D in 2026.

- Initial Enrollment Period (IEP): Seven-month window around your 65th birthday.

- Annual Enrollment Period (AEP): October 15 – December 7, for changes effective January 1.

- Special Enrollment Periods (SEPs): Available for specific life events, such as moving or losing other coverage.

Special Enrollment Periods (SEPs) allow you to make changes outside of the AEP under specific circumstances, such as moving to a new service area, losing other creditable drug coverage, or qualifying for Extra Help. It’s important to be aware of these periods and to act promptly if you experience a qualifying life event. Staying informed about these enrollment windows ensures seamless and appropriate prescription drug coverage.

Maximizing Your Medicare Part D Benefits: Tips for 2026

Once you’ve enrolled in a Medicare Part D plan for 2026, there are several strategies you can employ to maximize your benefits and manage your prescription drug costs effectively throughout the year. Being proactive and informed can lead to significant savings and better health outcomes.

One of the most effective strategies is to regularly review your medications with your doctor. Discuss whether generic alternatives are available for your brand-name drugs, as generics are almost always less expensive. Additionally, ask your doctor if they can prescribe a 90-day supply of maintenance medications instead of 30-day supplies, as this can sometimes reduce co-pays and trips to the pharmacy.

Utilizing Pharmacy Networks and Extra Help

Most Part D plans have preferred pharmacy networks where you can get your medications at a lower cost. Always check if your preferred pharmacy is in your plan’s network. If you have limited income and resources, you might qualify for Extra Help (also known as the Low-Income Subsidy), a Medicare program that helps pay for Part D premiums, deductibles, and co-payments. This can significantly reduce your out-of-pocket expenses.

- Generic Alternatives: Discuss with your doctor to save on costs.

- 90-Day Supplies: Consider for maintenance medications to reduce co-pays.

- Preferred Pharmacy Networks: Use in-network pharmacies for lower costs.

- Extra Help Program: Apply if eligible for assistance with Part D costs.

Furthermore, keep track of your medication costs and review your Explanation of Benefits (EOB) statements from your plan to ensure accuracy. If you notice discrepancies or have questions, contact your plan directly. By actively managing your Part D benefits, you can ensure you’re getting the most out of your prescription drug coverage in 2026 and keeping your healthcare costs in check.

| Key Aspect | Brief Description |

|---|---|

| Cost Components | Premiums, deductibles, co-pays, and coinsurance vary by plan and impact total out-of-pocket costs. |

| Formulary Importance | The list of covered drugs and their cost tiers is crucial for ensuring your medications are affordable. |

| Coverage Phases | Understand deductible, initial coverage, coverage gap (donut hole), and catastrophic coverage for overall costs. |

| 2026 Updates | New $2,000 annual out-of-pocket cap and reduced costs in the coverage gap offer significant financial protection. |

Frequently Asked Questions About Medicare Part D in 2026

The main goal of Medicare Part D in 2026 is to help beneficiaries manage the costs of prescription drugs. It provides coverage through private insurance plans approved by Medicare, aiming to make medications more affordable and accessible, especially with new cost caps.

To compare plans effectively, use the Medicare Plan Finder tool on the official Medicare website. Enter your specific medications to get personalized cost estimates. Also, consider consulting with SHIP (State Health Insurance Assistance Program) for unbiased, expert guidance.

The $2,000 out-of-pocket cap for 2026 means that once your annual spending on covered prescription drugs reaches this amount, you will pay nothing for your medications for the rest of the year. This significantly enhances financial protection for beneficiaries with high drug costs.

Yes, a Part D plan’s formulary can change during the year. However, plans are required to notify you if a drug you are currently taking is removed from the formulary or moved to a higher cost-sharing tier. You can also request a formulary exception.

The Annual Enrollment Period (AEP) for Medicare Part D runs from October 15 to December 7 each year. During this time, you can join a new plan, switch plans, or drop your current coverage, with any changes taking effect on January 1 of the following year.

Conclusion

Navigating Medicare Part D in 2026: Comparing Plans and Finding the Best Prescription Drug Coverage for You is a critical task that demands careful attention and informed decision-making. By understanding the core components of Part D, including premiums, deductibles, formularies, and the new out-of-pocket cap, beneficiaries can effectively evaluate their options. Utilizing resources like the Medicare Plan Finder and seeking expert advice ensures you select a plan that not only covers your necessary medications but also aligns with your financial situation. Proactive engagement with your plan and healthcare providers can further optimize your benefits, leading to better health outcomes and greater peace of mind in managing your prescription drug costs.