Navigating 2026 FAFSA Changes: A Family’s Step-by-Step Guide

Advertisers

Families need to understand the significant updates to the 2026 FAFSA, which include a simplified application, new eligibility criteria, and changes to aid calculations, requiring proactive planning to maximize financial assistance for higher education.

Advertisers

Preparing for college is a monumental task, and for many families, securing financial aid is a critical component of that journey. The Free Application for Federal Student Aid (FAFSA) is the gateway to federal grants, scholarships, and loans, but the upcoming 2026 FAFSA Changes introduce a new landscape that requires careful navigation. This comprehensive guide offers practical solutions and a step-by-step walkthrough to help families understand and adapt to these pivotal modifications, ensuring they are well-prepared to maximize their financial aid opportunities.

Understanding the Core 2026 FAFSA Changes

The FAFSA is undergoing its most significant overhaul in decades, aiming to streamline the application process and expand eligibility for federal student aid. These changes, part of the FAFSA Simplification Act, will impact how families apply for aid, how aid is calculated, and ultimately, how much assistance students receive. It’s crucial for families to grasp these fundamental shifts early to plan effectively.

Advertisers

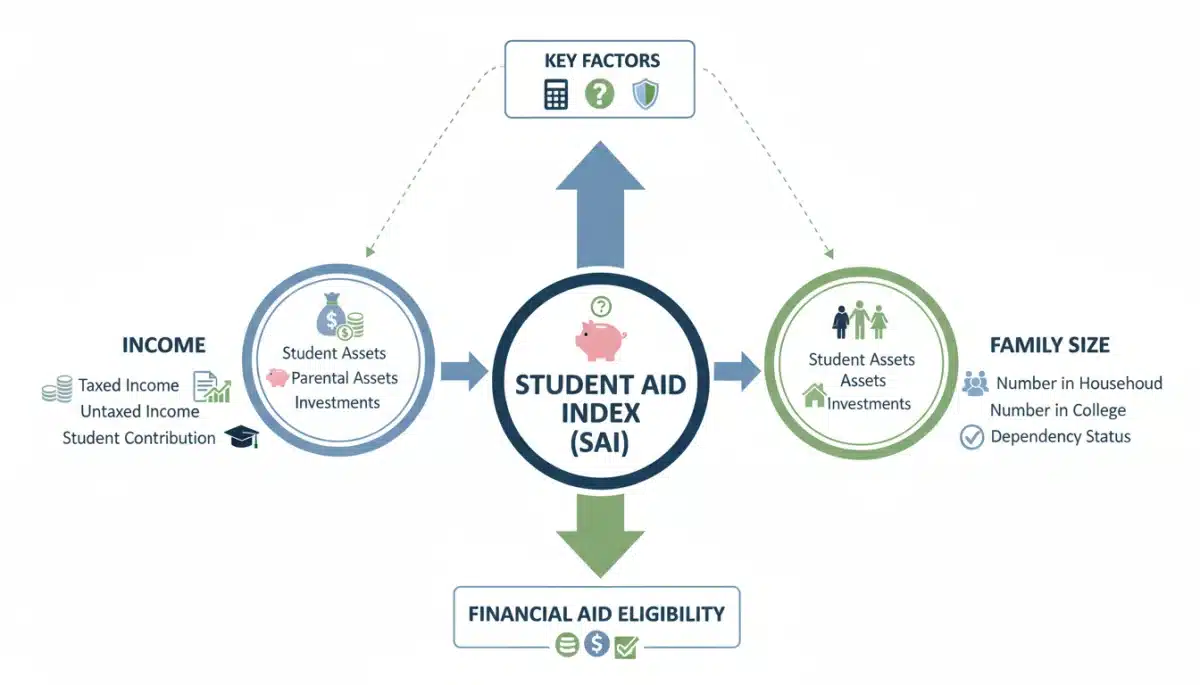

At the heart of the reform is the replacement of the Expected Family Contribution (EFC) with the Student Aid Index (SAI). This new metric is designed to be a more accurate assessment of a family’s ability to pay for college. Additionally, the application itself will be significantly shorter and more user-friendly, reducing the burden on applicants. However, simplicity doesn’t always mean straightforward for everyone, and certain aspects require particular attention.

Key Shifts in Terminology and Calculation

One of the immediate changes families will notice is the new terminology. The EFC, a familiar term for generations, is being replaced by the SAI. While both aim to determine aid eligibility, the SAI calculation incorporates different methodologies, which could lead to varying aid outcomes for individual families.

- Student Aid Index (SAI): Replaces the Expected Family Contribution (EFC) as the primary indicator of a student’s financial need. Unlike EFC, the SAI can be a negative number, indicating a higher level of need.

- Simplified Application: The number of questions on the FAFSA has been significantly reduced, making the application process faster and less daunting.

- Direct Data Exchange: A more direct transfer of federal tax information from the IRS will simplify the income reporting process, reducing errors and saving time.

These changes are designed to make the process more equitable and efficient, but understanding the nuances of the SAI calculation, especially regarding assets and income, is vital. Families should familiarize themselves with how their specific financial situation might be viewed under the new system.

Step-by-Step Guide to the New FAFSA Application Process

Navigating the updated FAFSA application process for 2026 requires a methodical approach. While the aim is simplification, being prepared with the right information and understanding each step will ensure a smoother experience. This section outlines the essential steps families should take to complete the FAFSA accurately and efficiently.

The new FAFSA is expected to be more intuitive, but gathering all necessary documents beforehand remains a critical first step. This includes tax returns, records of untaxed income, and information on assets. Even with direct data exchange, having these documents on hand can help verify information and answer any specific questions that may arise during the application.

Gathering Essential Documents

Before even logging into the FAFSA portal, compile all relevant financial documents. This proactive step can prevent delays and reduce stress during the application process.

- Federal Tax Returns: For the student and parents (if applicable) from the prior-prior year. For the 2026-2027 FAFSA, this will typically be 2024 tax information.

- Records of Untaxed Income: Such as child support received, interest income, and veterans’ non-education benefits.

- Asset Information: Current balances of cash, savings, checking accounts, and investments (excluding retirement accounts).

Ensuring all documents are readily available will significantly expedite the application process, allowing families to focus on accuracy rather than scrambling for information. This preparation is a cornerstone of a successful FAFSA submission.

Understanding the Student Aid Index (SAI) Calculation

The transition from EFC to SAI is arguably the most impactful change for families seeking federal financial aid. The SAI is not a dollar amount that families are expected to pay, but rather an index number used by financial aid administrators to determine the amount of federal student aid a student is eligible to receive. A lower SAI indicates a greater financial need and potentially more aid.

The calculation for the SAI takes into account several factors, including parent and student income, assets, and family size. Notably, the new formula removes the number of family members in college from the calculation, which could impact families with multiple children pursuing higher education simultaneously. Understanding these elements is key to estimating potential aid.

One significant change is how family businesses and farms are treated. Previously, these assets were often excluded for certain thresholds; under the new rules, these assets may be included in the SAI calculation, potentially affecting aid eligibility for some families. It’s crucial to review these specific asset inclusions carefully.

Impact of Income and Assets on SAI

The way income and assets are weighed in the SAI calculation has been refined. While income generally has a greater impact than assets, understanding the specific thresholds and allowances is important.

- Income Assessment: The formula will continue to assess a portion of both parent and student income. There are allowances for taxes and basic living expenses.

- Asset Protection Allowance: The amount of assets protected from the SAI calculation has increased, which could benefit some families by reducing their assessed financial strength.

- Exclusion of Certain Assets: Retirement accounts, the value of life insurance, and certain small businesses or family farms may be treated differently or excluded, depending on specific criteria.

Families should carefully evaluate their financial portfolios, particularly regarding assets, to understand how they will contribute to their student’s SAI. Strategic financial planning well in advance of the FAFSA application can make a difference in aid eligibility.

Maximizing Your Financial Aid Opportunities

Beyond simply completing the FAFSA, families can employ several strategies to maximize their financial aid opportunities under the new 2026 guidelines. Proactive planning and a thorough understanding of the aid landscape are essential. This includes not only federal aid but also state, institutional, and private scholarships.

One often-overlooked aspect is understanding the cost of attendance (COA) at various institutions. While the FAFSA determines eligibility for federal aid, individual colleges may have different policies for distributing institutional aid. Researching these policies and understanding how they interact with federal aid can significantly impact the overall cost of college.

Strategies for Optimizing Aid Eligibility

Several strategies can help families optimize their aid eligibility, ranging from financial adjustments to careful application practices.

- Early Application: Submitting the FAFSA as early as possible after it opens increases the chances of receiving aid, as some funds are distributed on a first-come, first-served basis.

- Understanding Professional Judgment: If a family’s financial situation has changed significantly since the tax year used for the FAFSA (e.g., job loss, medical expenses), they can appeal to the financial aid office for a professional judgment review.

- Researching Scholarships: Actively search for and apply to external scholarships from private organizations, which do not need to be repaid and can significantly reduce college costs.

By taking a comprehensive approach that includes timely application, understanding the appeals process, and seeking out additional funding sources, families can significantly enhance their chances of receiving the maximum possible financial assistance.

Common Pitfalls and How to Avoid Them

Even with a simplified FAFSA, common pitfalls can hinder a family’s financial aid prospects. Being aware of these potential issues and knowing how to avoid them is just as important as understanding the new rules. From incorrect data entry to missed deadlines, small mistakes can have significant consequences.

One frequent error is failing to complete the FAFSA accurately. While the new form aims to reduce errors through direct data exchange, families must still review all pre-filled information carefully. Any discrepancies could lead to delays or incorrect aid calculations, requiring additional time and effort to correct.

Avoiding Costly Mistakes

Proactive measures can help families steer clear of common FAFSA-related problems, ensuring a smooth application process and accurate aid determination.

- Double-Check All Information: Even with IRS data retrieval, manually verify all information for accuracy before submission.

- Meet Deadlines: Be aware of federal, state, and institutional FAFSA deadlines. Missing a deadline can mean missing out on crucial aid.

- Understand Dependency Status: Incorrectly reporting a student’s dependency status is a common error that can significantly impact aid eligibility. Consult the FAFSA guidelines carefully.

Paying close attention to detail and understanding the specific requirements for each section of the FAFSA can prevent unnecessary complications and ensure that families receive the aid they are entitled to.

Long-Term Financial Planning for College

Beyond the immediate FAFSA application, long-term financial planning is paramount for families preparing for college. The 2026 FAFSA changes underscore the importance of continuous financial literacy and strategic savings. Starting early and understanding how various savings vehicles impact financial aid can make a substantial difference in reducing the overall cost of higher education.

Families should consider how their assets are held and how different investment strategies might affect the SAI. For instance, certain types of savings accounts are treated more favorably than others in financial aid calculations. A well-thought-out financial plan can significantly mitigate college expenses over time.

Strategic Savings and Investment Approaches

Exploring various savings and investment options can help families prepare for college while potentially optimizing their financial aid eligibility.

- 529 Plans: These college savings plans are generally treated as a parent’s asset, which has a lesser impact on financial aid eligibility compared to student-owned assets.

- Custodial Accounts (UGMA/UTMA): While these accounts offer flexibility, assets held in a student’s name can have a more significant impact on their SAI.

- Retirement Accounts: Funds in qualified retirement accounts (e.g., 401(k)s, IRAs) are generally not counted as assets in the FAFSA calculation.

Consulting with a financial advisor specializing in college planning can provide tailored advice and help families develop a robust long-term strategy that aligns with their financial goals and aid eligibility considerations.

The Role of Communication and Resources

Effective navigation of the 2026 FAFSA changes hinges heavily on open communication and leveraging available resources. Families should maintain clear lines of communication with financial aid offices, guidance counselors, and, if applicable, financial advisors. These professionals can offer invaluable insights and assistance tailored to individual circumstances.

The Department of Education and various educational organizations continually update their resources to reflect the latest FAFSA information. Staying informed through official channels and engaging with support networks can help demystify complex aspects of the financial aid process.

Key Resources and Support Systems

Knowing where to turn for help and reliable information is crucial for families navigating the evolving financial aid landscape.

- Federal Student Aid Website: The official source for FAFSA information, updates, and application portals.

- College Financial Aid Offices: Direct contact with the financial aid office at prospective colleges can provide institution-specific guidance and clarification on policies.

- High School Guidance Counselors: Often equipped with up-to-date information and resources, guidance counselors can offer personalized advice and support during the application process.

Proactive engagement with these resources ensures that families receive accurate, timely, and personalized assistance, empowering them to make informed decisions regarding college financing. Open dialogue and seeking expert advice are indispensable tools in this journey.

| Key Point | Brief Description |

|---|---|

| SAI Replaces EFC | The Student Aid Index (SAI) replaces Expected Family Contribution (EFC) for determining financial need, with a new calculation methodology. |

| Simplified Application | The 2026 FAFSA form will be shorter and more user-friendly, with fewer questions and direct IRS data exchange. |

| New Aid Eligibility | Changes in the SAI calculation, including asset treatment, may impact how much federal aid families are eligible for. |

| Proactive Planning | Families should gather documents early, understand SAI impact, and explore all aid sources to maximize opportunities. |

Frequently Asked Questions About 2026 FAFSA

The most significant change is the replacement of the Expected Family Contribution (EFC) with the Student Aid Index (SAI). This new metric will be used to determine a student’s eligibility for federal financial aid, with different calculation methodologies that could alter aid outcomes for many families.

The 2026 FAFSA introduces changes to how assets are considered. Notably, family businesses and farms may now be included in the SAI calculation, which was not always the case previously. However, the asset protection allowance has also increased, potentially benefiting some families.

Yes, you will still need to provide tax information. However, the process is streamlined through a direct data exchange with the IRS. This aims to reduce errors and simplify reporting, but applicants should still review pre-filled data carefully for accuracy.

Under the new SAI calculation, the number of family members enrolled in college will no longer be a factor. This is a significant departure from the previous EFC formula, which often provided more aid to families with multiple college students.

Families should begin preparing as early as possible. This includes gathering prior-prior year tax documents, understanding the new SAI calculation, and researching potential institutional aid and scholarships. Early preparation can prevent last-minute stress and improve aid outcomes.

Conclusion

The 2026 FAFSA Changes represent a significant evolution in federal student aid, designed to simplify the application process and expand access to financial assistance. While these reforms aim for greater equity and efficiency, they also necessitate a proactive and informed approach from families. By understanding the shift from EFC to SAI, meticulously preparing all required documentation, and actively seeking out all available resources, families can confidently navigate this new landscape. Strategic long-term financial planning, coupled with timely and accurate application submissions, will be the cornerstones of maximizing financial aid opportunities, ensuring that the dream of higher education remains accessible for students across the nation.