FSA vs. HSA in 2026: Maximize Family Health Savings

Advertisers

Understanding the nuanced differences between a Flexible Spending Account (FSA) and a Health Savings Account (HSA) in 2026 is paramount for families seeking to optimize their healthcare spending and unlock significant tax benefits.

As we navigate the evolving landscape of healthcare in 2026, families face increasingly complex decisions regarding their health benefits. One of the most common dilemmas involves choosing between a Flexible Spending Account (FSA) and a Health Savings Account (HSA). Understanding the intricacies of FSA vs. HSA in 2026: Which Health Benefit Account Offers More Tax Advantages for Your Family? is not just about saving money; it’s about strategic financial planning for your family’s well-being. This guide will help you decipher which option aligns best with your unique healthcare needs and financial goals.

Advertisers

Understanding Flexible Spending Accounts (FSA) in 2026

A Flexible Spending Account (FSA) allows employees to set aside pre-tax money from their paycheck to pay for qualified out-of-pocket healthcare costs. This account is typically offered by employers and can be a fantastic way to save on taxes while covering medical, dental, and vision expenses for you and your dependents.

In 2026, FSAs continue to be a popular choice for many, especially those with predictable healthcare expenses. The primary benefit lies in the tax savings, as contributions are exempt from federal income tax, Social Security, and Medicare taxes, effectively reducing your taxable income.

Advertisers

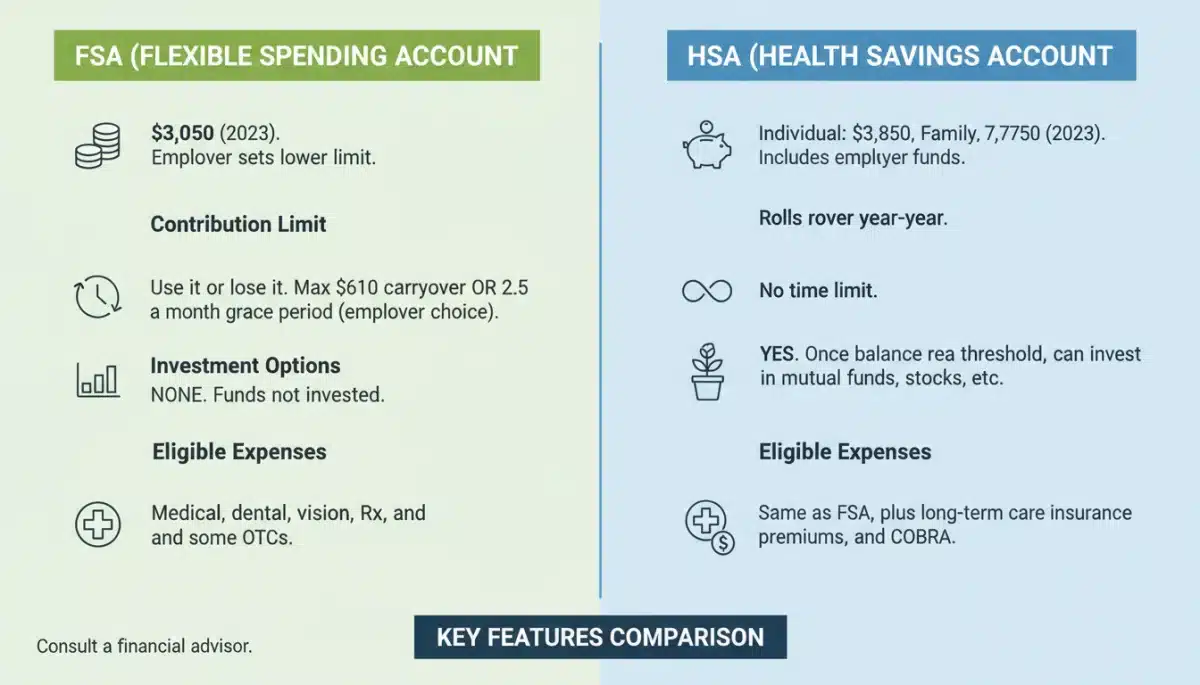

Contribution Limits and Eligible Expenses

The IRS sets annual contribution limits for FSAs, which are subject to inflation adjustments each year. For 2026, it’s crucial to check the most current limits to plan your contributions accurately. These funds can be used for a wide array of eligible expenses, from co-payments and deductibles to prescription medications and even some over-the-counter items.

- Tax Savings: Contributions are pre-tax, reducing your overall taxable income.

- Broad Eligibility: Covers medical, dental, vision, and often dependent care expenses.

- Immediate Access: The full elected amount is typically available on the first day of the plan year.

The ‘Use-It-or-Lose-It’ Rule

One of the most significant characteristics of an FSA is the ‘use-it-or-lose-it’ rule. This means that funds not used by the end of the plan year are generally forfeited. However, some employers offer grace periods or limited carryover options, allowing a small portion of unused funds to roll over to the next year. It’s essential to understand your employer’s specific FSA rules to avoid losing your hard-earned money.

Despite this potential drawback, FSAs remain highly valuable for families with consistent healthcare needs. The upfront tax savings can be substantial, making healthcare more affordable. Proper planning of anticipated expenses is key to maximizing an FSA’s benefits.

In conclusion, FSAs provide a tax-advantaged way to pay for current healthcare costs, offering immediate financial relief. Careful estimation of annual medical expenses is vital to fully leverage this account and avoid the forfeiture of funds at year-end.

Exploring Health Savings Accounts (HSA) in 2026

A Health Savings Account (HSA) is a tax-advantaged savings account that can be used for healthcare expenses, but it comes with a crucial prerequisite: you must be enrolled in a High-Deductible Health Plan (HDHP). HSAs are unique because they offer a triple tax advantage, making them a powerful tool for long-term health savings and retirement planning.

For families in 2026, an HSA can represent a significant financial opportunity. Unlike FSAs, HSAs are owned by the individual, not the employer, meaning the account is portable and stays with you even if you change jobs or retire.

Triple Tax Advantage and Investment Potential

The ‘triple tax advantage’ of an HSA refers to:

- Tax-deductible contributions: Money you contribute is subtracted from your taxable income.

- Tax-free growth: Your funds grow tax-free, and you can often invest them once a certain balance is reached.

- Tax-free withdrawals: Funds withdrawn for qualified medical expenses are tax-free.

This investment potential sets HSAs apart. Once your balance reaches a certain threshold, often around $1,000, you can typically invest your HSA funds in various options, similar to a 401(k) or IRA. This allows your healthcare savings to grow over time, potentially providing a substantial nest egg for future medical costs, especially in retirement.

Eligibility and Contribution Limits

To be eligible for an HSA in 2026, you must be covered by an HDHP and not be enrolled in Medicare, nor be claimed as a dependent on someone else’s tax return. The IRS also sets annual contribution limits for HSAs, with separate limits for individuals and families, which are adjusted for inflation. These limits are typically higher than FSA limits, allowing for greater savings.

The flexibility of an HSA, combined with its powerful tax advantages and investment opportunities, makes it an attractive option for those who can afford an HDHP and want to plan for both short-term and long-term healthcare needs. It’s a savings vehicle that truly offers lasting benefits.

In summary, HSAs are excellent for individuals and families looking for a tax-advantaged way to save for current and future medical expenses, particularly those comfortable with an HDHP and seeking investment growth potential.

Key Differences: FSA vs. HSA in 2026

While both FSAs and HSAs offer tax advantages for healthcare expenses, their fundamental structures, eligibility requirements, and long-term implications differ significantly. Understanding these distinctions is crucial for making an informed decision for your family in 2026.

One of the most prominent differences lies in their relationship with health insurance plans. An HSA absolutely requires enrollment in a High-Deductible Health Plan (HDHP), whereas an FSA can be paired with almost any health insurance plan. This initial barrier to entry for HSAs means not everyone is eligible, regardless of their desire to save.

Ownership and Portability

HSAs are individually owned accounts, meaning the funds belong to you, not your employer. This makes them portable; you can take your HSA with you if you change jobs or retire. The money remains yours indefinitely. In contrast, FSAs are employer-sponsored plans, and while some employers offer limited carryover, the funds are generally tied to your employment and typically forfeited if unused by year-end or upon leaving the company.

- HSA Ownership: Individual, portable, funds roll over year to year.

- FSA Ownership: Employer-sponsored, generally ‘use-it-or-lose-it’ with limited exceptions.

Investment Potential and Long-Term Savings

Another critical divergence is the investment potential. HSAs allow you to invest your funds, similar to a retirement account, enabling tax-free growth over time. This makes HSAs a powerful long-term savings and retirement vehicle. FSAs, on the other hand, are spending accounts; funds are meant to be used within the plan year and do not offer investment options.

For families considering their financial future, the ability to invest HSA funds can be a game-changer, providing a substantial pool of money for healthcare expenses later in life, even well into retirement. This long-term growth potential is a major differentiator when comparing FSA vs. HSA in 2026.

In essence, while FSAs are excellent for covering immediate, predictable healthcare costs with pre-tax dollars, HSAs offer a more robust, long-term savings and investment strategy for those who meet the HDHP requirement.

Tax Advantages Compared: Which is Better for Your Family?

Both FSAs and HSAs offer attractive tax benefits, but the nature and extent of these advantages vary, making one potentially more suitable than the other depending on your family’s financial situation and healthcare usage. Understanding these specific tax implications is paramount for maximizing your savings in 2026.

The primary tax advantage of both accounts is that contributions are made with pre-tax dollars, reducing your taxable income. This immediate tax break can lead to significant savings on federal income tax, and often state income tax, as well as FICA taxes (Social Security and Medicare).

FSA Tax Benefits: Immediate Savings

With an FSA, you contribute pre-tax dollars, which means your contributions are deducted from your gross pay before taxes are calculated. This immediately lowers your taxable income, resulting in a smaller tax bill for the current year. The funds are then used to pay for qualified medical expenses tax-free.

- Pre-tax contributions: Reduces current year’s taxable income.

- Tax-free withdrawals: For qualified medical expenses.

- No FICA taxes: Contributions are exempt from Social Security and Medicare taxes.

This immediate reduction in taxable income is particularly appealing for families with regular, predictable healthcare costs, as they can confidently allocate funds knowing they will be utilized within the plan year.

HSA Tax Benefits: Triple Advantage and Long-Term Growth

HSAs provide a ‘triple tax advantage’ that offers more extensive long-term benefits. Contributions are tax-deductible (if made directly) or pre-tax (if through payroll deduction), funds grow tax-free, and withdrawals for qualified medical expenses are also tax-free. Furthermore, after age 65, HSA funds can be withdrawn for any purpose without penalty, though non-medical withdrawals will be taxed as ordinary income.

This long-term growth potential, combined with the ability to invest funds, positions HSAs as a powerful retirement savings vehicle. For families who can afford to pay for current medical expenses out-of-pocket and let their HSA funds grow, the tax advantages are substantial and compound over time. When evaluating FSA vs. HSA in 2026, the HSA’s ability to serve as a supplemental retirement account for healthcare costs is a significant differentiator.

In summary, FSAs offer immediate tax relief on current healthcare spending, while HSAs provide a more comprehensive, long-term tax-advantaged savings and investment strategy, making them highly attractive for future financial security.

Who Benefits More: Families with Predictable vs. Unpredictable Healthcare Needs

The choice between an FSA and an HSA in 2026 largely hinges on your family’s healthcare predictability. Families with consistent, foreseeable medical expenses will likely find one option more advantageous, while those with unpredictable or minimal current healthcare needs might prefer the other.

Understanding your family’s typical healthcare utilization is the first step in determining which account will offer the most benefit. This involves reviewing past medical expenses, considering any chronic conditions, and anticipating future needs like orthodontics or planned surgeries.

FSA for Predictable Expenses

For families with predictable healthcare costs, an FSA often shines. If you know you’ll have regular doctor visits, ongoing prescriptions, or planned dental work, an FSA allows you to budget for these expenses with pre-tax dollars. The ‘use-it-or-lose-it’ rule becomes less of a concern when you have a clear understanding of your annual medical spending.

- Known Costs: Ideal for families with recurring medical, dental, or vision expenses.

- Dependent Care FSA: A separate FSA specifically for childcare expenses, which can be a huge benefit for working parents.

- No HDHP Required: Accessible to a broader range of insurance plans.

This makes FSAs particularly appealing for young families with children who might have frequent doctor visits or families managing chronic conditions where expenses are relatively stable year-to-year.

HSA for Unpredictable or Minimal Expenses and Long-Term Savings

Conversely, families with generally good health and low, unpredictable medical expenses, or those who can comfortably cover their high deductible, are prime candidates for an HSA. The ability to roll over funds year after year, invest them, and build a substantial tax-free savings for future healthcare needs is invaluable.

Even if you have a year with higher-than-expected medical costs, the HSA acts as a robust savings vehicle. You can pay for qualifying expenses from your HSA or even pay out-of-pocket and reimburse yourself later, allowing your funds to continue growing tax-free. This flexibility and long-term perspective are key advantages when considering FSA vs. HSA in 2026 for future-focused families.

Ultimately, the decision rests on a realistic assessment of your family’s health and financial strategy. FSAs provide immediate relief for known expenses, while HSAs offer a powerful, flexible savings tool for both unforeseen costs and long-term financial planning.

Strategic Planning for Your Family’s Healthcare in 2026

Making the right choice between an FSA and an HSA in 2026 requires careful strategic planning. It’s not a one-size-fits-all decision, and what works best for one family might not be ideal for another. Your family’s current health status, financial goals, and risk tolerance all play significant roles.

Begin by thoroughly reviewing your family’s health insurance options for 2026. If an HDHP is not available or not suitable for your family’s needs, then an HSA is not an option, making an FSA the primary choice for tax-advantaged healthcare spending.

Assessing Your Family’s Healthcare Needs

Consider the following questions when evaluating your family’s healthcare needs:

- Do any family members have chronic conditions requiring regular medication or specialist visits?

- Are you planning for significant medical events, such as surgery, orthodontics, or expanding your family?

- What were your out-of-pocket medical expenses in previous years?

Answering these questions will help you estimate your anticipated annual healthcare costs, which is crucial for determining how much to contribute to an FSA to avoid the ‘use-it-or-lose-it’ scenario, or if an HDHP and HSA might be more cost-effective in the long run.

Considering Long-Term Financial Goals

For families focused on long-term financial security and retirement planning, the HSA’s investment potential is a major draw. The ability to grow funds tax-free and withdraw them tax-free for qualified medical expenses, even in retirement, provides a significant advantage. It can act as an additional retirement savings vehicle specifically earmarked for healthcare costs, which often increase with age.

Conversely, if your immediate financial priority is to reduce current taxable income and manage predictable healthcare expenses without the complexities of investment, an FSA offers a straightforward and effective solution. When comparing FSA vs. HSA in 2026, consider whether your priority is immediate tax savings on known expenses or building a substantial, flexible fund for future healthcare.

Ultimately, a comprehensive review of your family’s health, financial situation, and future aspirations will guide you to the optimal health benefit account. Don’t hesitate to consult with a financial advisor to tailor a strategy that best suits your unique circumstances.

Maximizing Benefits: Tips for Both FSA and HSA Users

Regardless of whether you choose an FSA or an HSA, there are strategies you can employ to maximize the benefits and ensure you’re getting the most out of your chosen account. Effective management is key to leveraging these tax-advantaged tools for your family’s health and financial well-being in 2026.

For both account types, meticulous record-keeping of all medical expenses and receipts is paramount. This ensures you can justify withdrawals for qualified expenses, especially during an audit, and helps you track your spending against your contributions.

Tips for FSA Users

To make the most of your FSA and avoid the ‘use-it-or-lose-it’ pitfall:

- Estimate Carefully: Review past medical expenses and anticipate future needs to contribute an amount you’re confident you’ll spend.

- Utilize the Grace Period/Carryover: Understand your employer’s specific rules. If there’s a grace period, plan to spend remaining funds during that time.

- Stock Up on Eligible Items: Towards the end of the plan year, use any remaining balance on eligible over-the-counter medications, first-aid supplies, or even new eyeglasses/contacts.

Proactive planning and spending are crucial for FSA success. Don’t wait until the last minute to use your funds; integrate your FSA into your regular healthcare budgeting throughout the year.

Tips for HSA Users

HSAs offer more flexibility, but strategic management can still enhance their value:

- Maximize Contributions: If possible, contribute the maximum allowed each year to take full advantage of the triple tax benefits and investment potential.

- Invest Your Funds: Once you have a comfortable emergency buffer in cash, explore the investment options offered by your HSA provider to grow your savings.

- Pay Out-of-Pocket (If Possible): If you can afford to pay for current medical expenses from your regular checking account, do so. This allows your HSA funds to continue growing tax-free, and you can reimburse yourself years later, tax-free.

- Keep all Receipts: Even if you don’t reimburse yourself immediately, keep receipts for all qualified medical expenses. You can use these later to withdraw funds tax-free from your HSA, even in retirement.

By adopting these strategies, families can significantly enhance the financial impact of both FSAs and HSAs, ensuring their healthcare dollars work harder for them in 2026 and beyond.

| Key Feature | FSA (Flexible Spending Account) | HSA (Health Savings Account) |

|---|---|---|

| Eligibility | Any health plan offered by employer. | Must be enrolled in a High-Deductible Health Plan (HDHP). |

| Fund Rollover | Generally ‘use-it-or-lose-it’ with limited carryover or grace period. | Funds roll over year-to-year indefinitely. |

| Investment Options | No investment options; spending account only. | Funds can be invested for tax-free growth. |

| Portability | Tied to employment; typically lost upon leaving. | Owned by individual; portable if you change jobs or retire. |

Frequently Asked Questions About FSA vs. HSA in 2026

Generally, no. You cannot typically contribute to a standard FSA and an HSA at the same time. However, you might be eligible for a Limited-Purpose FSA (LPFSA), which covers vision and dental expenses, alongside an HSA. This combination allows for broader coverage.

HSA funds are yours to keep, regardless of employment changes, as you own the account. FSA funds, being employer-sponsored, are typically forfeited upon leaving your job, unless your employer offers COBRA extension for the FSA or a limited grace period.

Yes, under current regulations for 2026, most over-the-counter medications and products are eligible for reimbursement from both FSA and HSA accounts without a prescription. This includes items like pain relievers, cold medicines, and feminine hygiene products.

You can, but it’s generally not advisable before age 65. Withdrawals for non-medical expenses before age 65 are subject to income tax and a 20% penalty. After age 65, non-medical withdrawals are taxed as ordinary income but are not penalized, making it a flexible retirement savings tool.

HSA contribution limits are generally higher than FSA limits, allowing for greater tax-advantaged savings, especially for families. Both limits are adjusted annually by the IRS for inflation, so it’s important to check the specific figures for 2026 from official sources.

Conclusion

The decision between an FSA and an HSA in 2026 is a pivotal one for families aiming to optimize their healthcare spending and maximize tax advantages. While FSAs offer immediate tax relief for predictable, current medical expenses with a ‘use-it-or-lose-it’ caveat, HSAs provide a robust, portable, and investment-driven solution for long-term health savings, contingent on enrollment in an HDHP. By carefully assessing your family’s healthcare needs, financial goals, and consulting available resources, you can confidently choose the account that best secures your family’s health and financial future.