Inflation Outlook 2026: Fed Projects 2.5% Rate & Household Impact

Anúncios

The Federal Reserve projects a 2.5% inflation rate for the US economy in 2026, indicating a continued focus on price stability and directly influencing household budgets and investment strategies.

Anúncios

As we look towards the middle of the decade, understanding the inflation outlook 2026 is crucial for every American household. The Federal Reserve’s recent projections, hinting at a 2.5% inflation rate for the US economy, are more than just numbers; they are a compass for financial planning, impacting everything from your daily grocery bill to long-term savings.

Understanding the Federal Reserve’s 2.5% Projection

The Federal Reserve plays a pivotal role in shaping the economic landscape of the United States. Their latest projection of a 2.5% inflation rate for 2026 is a carefully considered forecast, reflecting a balance between economic growth and price stability. This isn’t a random guess but a data-driven assessment, taking into account numerous economic indicators and global trends.

The Fed’s Mandate and Tools

The Federal Reserve operates with a dual mandate: to achieve maximum employment and maintain price stability. Inflation, when too high or too low, can disrupt this balance. A 2.5% target suggests the Fed believes this rate is conducive to healthy economic activity without eroding purchasing power too quickly.

Anúncios

- Monetary Policy: The Fed utilizes tools like interest rate adjustments, quantitative easing, and reserve requirements to influence the money supply and credit conditions.

- Economic Indicators: They closely monitor consumer price index (CPI), producer price index (PPI), employment data, and wage growth to make informed decisions.

- Forward Guidance: The Fed communicates its outlook and policy intentions to guide market expectations, which helps stabilize the economy.

This 2.5% projection isn’t a fixed certainty, but rather a central point in a range of possible outcomes. It reflects the Fed’s current assessment of how various economic forces are likely to evolve over the next few years, including supply chain dynamics, labor market conditions, and global economic stability. For households, this number serves as a critical benchmark for anticipating future costs and planning accordingly.

Recent updates in economic forecasts

Economic forecasts are dynamic, constantly refined as new data emerges and global events unfold. The Federal Reserve’s 2.5% inflation projection for 2026 is the latest in a series of updates, reflecting a nuanced understanding of current and anticipated economic conditions. These adjustments are crucial for businesses and individuals alike to make informed decisions.

Initially, post-pandemic inflation surged, leading to higher short-term expectations. However, with sustained efforts by the Fed and some normalization in global supply chains, the long-term outlook has begun to stabilize. The 2.5% figure suggests a belief that inflationary pressures will moderate from recent peaks but remain slightly above the traditional 2% target, indicating a cautious optimism about sustained economic growth.

Factors influencing the updated outlook

Several key factors contribute to the Fed’s revised forecasts. These include the ongoing resolution of supply chain bottlenecks, which reduce production costs, and a gradual rebalancing of labor markets, which can influence wage growth and consumer spending patterns.

- Global Energy Prices: Volatility in oil and gas markets continues to be a significant wild card, directly impacting transportation and manufacturing costs.

- Technological Advancements: Innovations in automation and efficiency can lead to deflationary pressures in certain sectors, balancing out other inflationary forces.

- Geopolitical Events: International conflicts or trade disputes can disrupt global markets, leading to sudden shifts in commodity prices and supply availability.

These recent updates underscore the complex interplay of domestic and international factors on the US economy. The 2.5% projection for 2026 is a testament to the Fed’s continuous analysis and adaptation to an ever-changing economic environment, providing a clearer, albeit still cautious, picture for future financial planning.

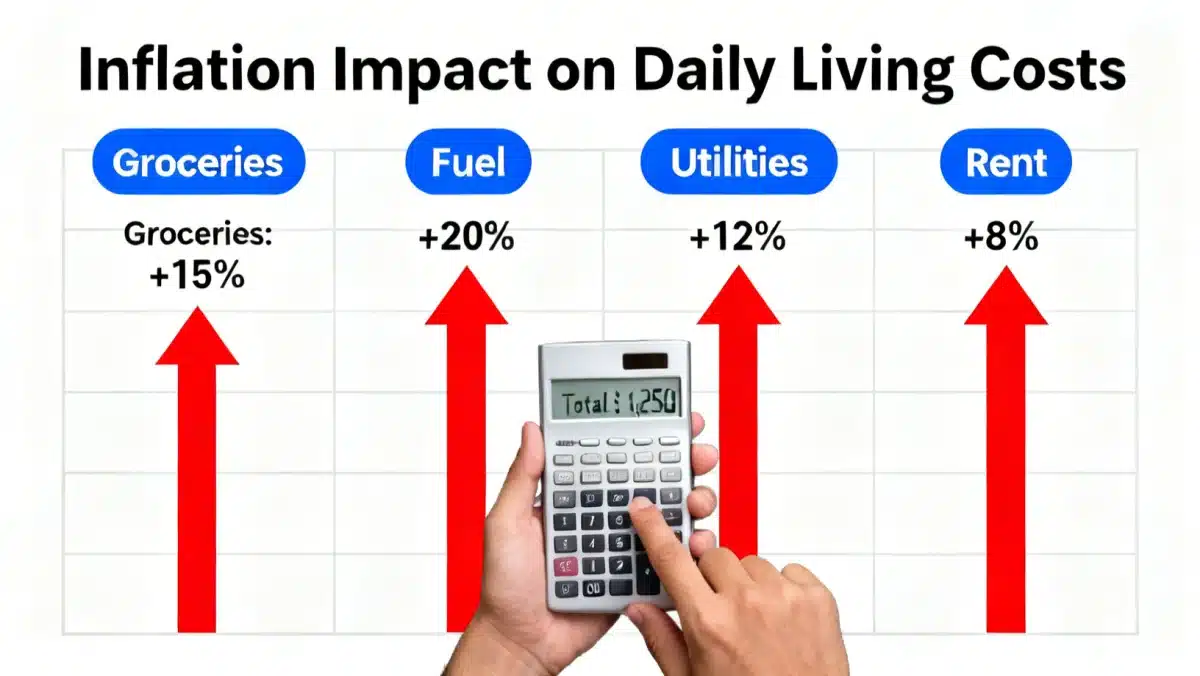

Impact on household budgets: what to expect

A 2.5% inflation rate, while seemingly modest, can have a noticeable cumulative effect on household budgets. This means that the purchasing power of your dollar will gradually decrease, making everyday goods and services more expensive over time. Understanding this impact is the first step towards mitigating its effects.

For many families, this translates into a need for careful budget adjustments. Categories such as groceries, transportation, and housing are often the first to feel the squeeze. While wages may also increase, they often lag behind inflation, creating a gap that requires strategic financial management to bridge.

Key areas of impact

The effects of inflation are not uniform across all spending categories. Some areas are more sensitive to price increases than others, requiring households to prioritize and adapt their spending habits.

- Groceries and Food: Food prices are highly susceptible to inflation due to factors like supply chain costs, weather patterns, and global commodity markets.

- Housing Costs: Rent and mortgage payments, property taxes, and utility bills can see significant increases, often forming the largest portion of a household budget.

- Transportation: Fuel prices, vehicle maintenance, and public transport fares are directly influenced by energy costs and broader economic conditions.

In essence, a 2.5% inflation rate means that what cost $100 today might cost $102.50 next year. Over several years, this can add up to a substantial increase in living expenses. Households will need to review their spending habits, seek ways to economize, and potentially explore opportunities to increase income to maintain their standard of living.

Strategies for managing personal finances

Navigating an inflationary environment requires proactive financial management. For families and individuals, developing robust strategies to cope with rising costs is essential to protect purchasing power and maintain financial stability. This involves a combination of smart spending, strategic saving, and informed investing.

The goal is not just to survive inflation but to thrive despite it. This means looking beyond immediate expenses and considering long-term financial health. Diversifying investments, optimizing debt, and ensuring adequate emergency savings are all critical components of an effective strategy.

Practical tips for households

Implementing concrete steps can make a significant difference in how well your household weathers inflationary pressures. Small changes can accumulate into substantial savings and better financial resilience.

- Budgeting and Tracking: Regularly review and adjust your budget to reflect rising costs. Track expenses to identify areas where you can cut back.

- Emergency Fund: Build or bolster an emergency fund covering 3-6 months of essential expenses. This provides a buffer against unexpected price hikes or income disruptions.

- Debt Management: Prioritize paying off high-interest debt, as its cost can increase during inflationary periods. Consider fixed-rate options for new loans.

- Smart Investing: Explore investments that historically perform well during inflation, such as real estate, commodities, or inflation-indexed bonds. Consult a financial advisor.

- Income Generation: Look for opportunities to increase your income, whether through negotiating salary increases, taking on freelance work, or developing new skills.

By adopting these strategies, households can build greater resilience against the impacts of inflation. It’s about being informed, proactive, and adaptable in your financial decisions, ensuring that your money continues to work for you even as prices rise.

The role of wages and employment in 2026

Wages and employment are inextricably linked to inflation. In 2026, as the Federal Reserve targets a 2.5% inflation rate, the dynamics of the labor market will play a crucial role in how effectively households can absorb rising costs. A robust job market with healthy wage growth can partially offset the erosion of purchasing power caused by inflation.

The expectation is that the labor market will continue to be relatively strong, albeit potentially cooling from the rapid growth seen in the immediate post-pandemic period. This balance is critical: too much wage growth can fuel further inflation, while too little can leave households struggling to keep up with expenses.

Labor market trends to watch

Several trends will shape the wage and employment landscape in 2026. These factors will influence job availability, salary negotiations, and overall economic stability for the average worker.

- Skill Gaps: Industries facing significant skill shortages may see higher wage growth as companies compete for talent.

- Automation and AI: The increasing adoption of automation and artificial intelligence could impact certain job sectors, requiring workers to adapt and reskill.

- Remote Work Flexibility: The continued prevalence of remote and hybrid work models could influence regional wage disparities and talent acquisition strategies.

For workers, understanding these trends can empower them to negotiate for better compensation and seek opportunities in high-demand fields. For employers, attracting and retaining talent will require competitive wage structures that account for inflationary pressures. Ultimately, a healthy equilibrium in the labor market is essential for both individual prosperity and broader economic stability in the face of a 2.5% inflation rate.

Long-term economic implications and outlook

Looking beyond 2026, the Federal Reserve’s projected 2.5% inflation rate has significant long-term economic implications. This rate, if sustained, suggests a period of moderate but persistent price increases, which will influence everything from investment returns to government fiscal policies. Understanding these broader trends is vital for long-term planning.

A consistent 2.5% inflation rate, while higher than the Fed’s historical 2% target, avoids the extremes of deflation (which can stifle economic activity) and hyperinflation (which can destabilize an economy). It implies a delicate balancing act by policymakers to foster growth without letting prices spiral out of control. This outlook shapes expectations for future interest rates, bond yields, and asset valuations.

Future considerations for policy and investment

The long-term economic outlook is influenced by various factors, requiring continuous monitoring and adaptation from both policymakers and investors. The sustained 2.5% inflation rate could lead to specific shifts in economic behavior.

- Fiscal Policy Alignment: Government spending and taxation policies will need to align with monetary policy to manage inflationary pressures and support sustainable growth.

- Retirement Planning: Individuals will need to adjust retirement savings goals to account for reduced purchasing power over decades, emphasizing growth-oriented investments.

- Corporate Investment: Businesses may prioritize investments in efficiency-enhancing technologies to offset rising labor and material costs, potentially boosting productivity.

In the long run, the 2.5% inflation outlook for 2026 suggests an economy that is growing, but one where vigilance against rising costs remains paramount. It underscores the need for individuals, businesses, and governments to adopt forward-thinking strategies to ensure sustained prosperity and financial resilience in the years to come.

| Key Point | Brief Description |

|---|---|

| Fed’s 2026 Projection | The Federal Reserve forecasts a 2.5% inflation rate for the US economy in 2026, indicating moderate price increases. |

| Household Budget Impact | Rising costs for groceries, housing, and transportation will necessitate budget adjustments and strategic financial planning. |

| Financial Strategies | Effective strategies include budgeting, emergency funds, debt management, and smart investing to mitigate inflation’s effects. |

| Long-Term Outlook | Sustained moderate inflation will influence retirement planning, corporate investments, and require aligned fiscal policies. |

Frequently asked questions about 2026 inflation

It means the Fed anticipates that the general price level for goods and services will increase by about 2.5% during 2026. This is a moderate rate, suggesting a stable but slightly higher inflation environment compared to their long-term 2% target, aiming for sustained economic growth without excessive price increases.

A 2.5% inflation rate will gradually increase the cost of living, meaning your money will buy slightly less over time. You can expect to pay more for essentials like groceries, housing, and fuel. It necessitates careful budgeting and potentially seeking ways to increase income to maintain your purchasing power.

To prepare, focus on smart budgeting, building an emergency fund, and managing debt effectively. Consider investments that historically perform well during inflation, such as real estate, commodities, or inflation-indexed bonds. Diversifying your portfolio and seeking financial advice are also beneficial steps.

Wage growth can vary significantly across industries and individual circumstances. While a strong labor market can support wage increases, they often lag behind inflation. It’s advisable to regularly assess your market value, negotiate salary increases, and explore opportunities for skill development to enhance your earning potential.

Long-term, a 2.5% inflation rate suggests an economy in a state of moderate growth, requiring ongoing vigilance from policymakers. It will influence retirement planning by necessitating higher savings, encourage corporate investments in efficiency, and demand alignment between fiscal and monetary policies to ensure stability and sustainable prosperity.

Conclusion

The Federal Reserve’s projection of a 2.5% inflation rate for the US economy in 2026 serves as a crucial benchmark for individuals, businesses, and policymakers alike. It signals a continued period of moderate price increases, necessitating proactive financial strategies and informed decision-making. While households will need to adapt to rising costs for everyday essentials, a robust labor market and strategic investments can help mitigate the impact. Understanding these dynamics is key to navigating the evolving economic landscape and fostering long-term financial resilience in the face of persistent, albeit controlled, inflationary pressures.