Long-Term Care Benefits 2026: Plan for Future Healthcare Costs

Advertisers

Understanding Long-Term Care Benefits 2026 is essential for proactively addressing the financial and logistical challenges associated with future healthcare needs, ensuring comprehensive planning for aging individuals and their families.

Preparing for the future is a cornerstone of financial stability, especially when it comes to healthcare. For many Americans, contemplating their long-term care needs can feel overwhelming. This article delves into Long-Term Care Benefits 2026: Planning Ahead for Future Healthcare Needs and Costs, offering a comprehensive guide to understanding what lies ahead and how to best prepare.

Advertisers

Understanding Long-Term Care: What It Entails

Long-term care refers to a range of medical and non-medical services provided to people who have a chronic illness or disability, preventing them from performing daily activities on their own. These services can be provided in various settings, including your home, assisted living facilities, or nursing homes. The need for long-term care can arise from aging, an accident, or an illness, and it’s a critical consideration for future planning.

As life expectancies increase, so does the likelihood of needing long-term care. It’s not just an issue for the elderly; a significant percentage of people under 65 also require some form of long-term care due to injury or illness. Understanding the scope of these services is the first step in effective planning.

Advertisers

Types of Long-Term Care Services

The spectrum of long-term care is broad, designed to meet diverse needs. It’s not a one-size-fits-all solution, and understanding the options helps in making informed decisions.

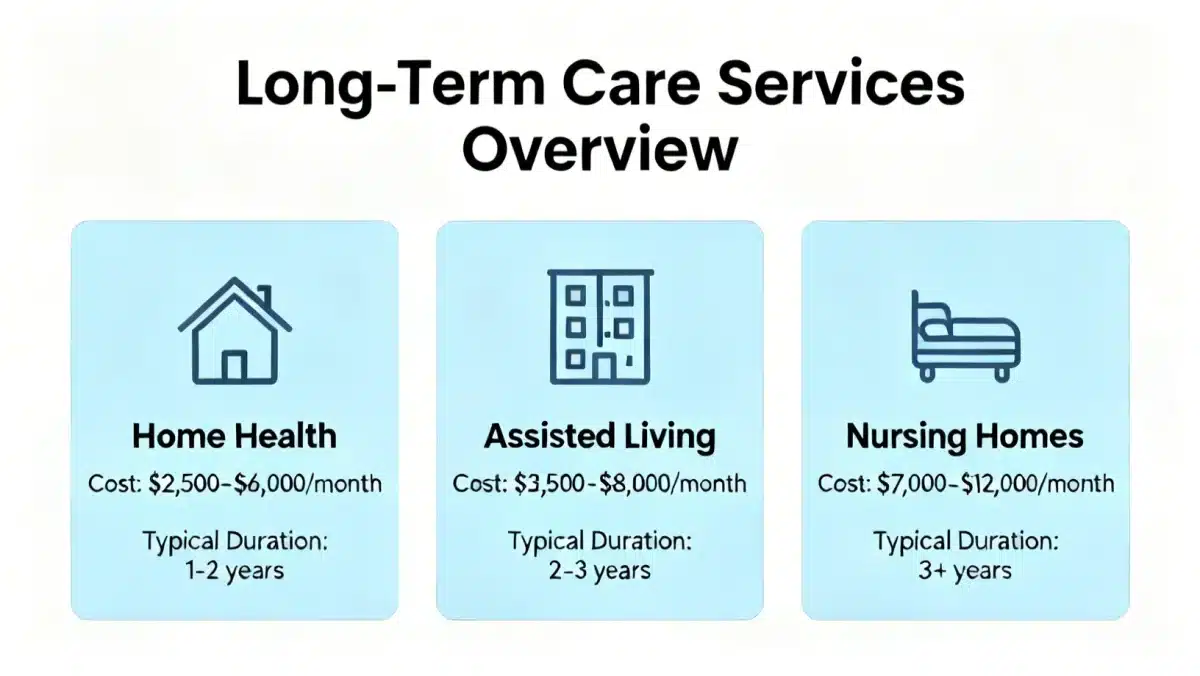

- Home Health Care: Services provided in the comfort of your home, including skilled nursing, therapy, and assistance with daily tasks.

- Assisted Living Facilities: Residential communities offering personal care support, meals, activities, and some medical supervision for those who need more help than home care can provide but don’t require 24/7 skilled nursing.

- Nursing Homes: Facilities providing 24-hour skilled nursing care, rehabilitation services, and assistance with daily living activities for individuals with complex medical needs.

- Adult Day Care: Programs offering supervised care, social activities, and health services in a community setting during the day, allowing caregivers to work or take a break.

Each type of care addresses different levels of need and comes with varying costs. Evaluating your potential future needs and preferences is vital for selecting the most appropriate option. This foresight is a key component of effective long-term care planning.

The Escalating Costs of Long-Term Care in 2026

The cost of long-term care is a significant concern for many families, and these costs are projected to continue rising by 2026. Without proper planning, these expenses can quickly deplete savings and assets, impacting not only the individual needing care but also their loved ones. Understanding the financial landscape is crucial for effective preparation.

Factors contributing to these escalating costs include inflation, increased demand for services, and the rising cost of labor for healthcare professionals. These trends underscore the importance of early and strategic financial planning to mitigate the burden.

Average Costs by Service Type

While exact figures can vary by location and provider, national averages give a general idea of the financial commitment involved. These numbers are projected to increase by 2026, making current planning even more critical.

- Home Health Aide: The median cost for a home health aide could be upwards of $60,000 per year, based on 44 hours per week.

- Assisted Living Facility: A private one-bedroom in an assisted living facility might cost around $55,000 to $65,000 annually.

- Nursing Home Care: A private room in a nursing home is often the most expensive option, potentially exceeding $100,000 to $120,000 per year.

These figures highlight the substantial financial challenge that long-term care presents. It’s important to research costs in your specific geographic area, as they can differ significantly. Proactive financial planning is the only way to effectively address these potential future expenses.

Government Programs and Their Role in 2026

While the costs of long-term care are significant, various government programs can offer assistance. However, it’s crucial to understand their limitations and eligibility requirements, as they rarely cover the full spectrum of long-term care expenses. These programs are often designed as a safety net, not a comprehensive solution for everyone.

Medicaid and Medicare are two primary federal programs that often come to mind, but their roles in long-term care are distinct and often misunderstood. Understanding these differences is key to determining what support might be available.

Medicare vs. Medicaid: Key Differences for Long-Term Care

Many believe Medicare will cover all their long-term care needs, but this is a common misconception. Medicare generally covers short-term skilled nursing care or home health care after a hospital stay, but not ongoing custodial care.

- Medicare: Primarily covers acute medical care, hospital stays, and limited skilled nursing facility care for a short period (up to 100 days) if certain conditions are met. It does not cover non-skilled personal care or long-term stays in assisted living or nursing homes.

- Medicaid: This is a state-federal program that provides healthcare coverage to low-income individuals and families. For long-term care, Medicaid can cover nursing home care, and in some states, home and community-based services, but it requires individuals to meet strict income and asset limits.

Beyond these, other state-specific programs or Veterans Affairs (VA) benefits might be available for eligible individuals. It’s essential to research and understand the specific criteria and benefits offered by these programs, as they can change and have strict eligibility rules. Relying solely on government programs without additional planning can leave significant gaps in coverage.

Private Long-Term Care Insurance: A Viable Option

For many, private long-term care insurance is a crucial component of a comprehensive financial plan. This type of insurance is designed specifically to cover the costs of long-term care services, providing a financial safety net that government programs often do not. It offers peace of mind by protecting assets and ensuring access to quality care.

Purchasing long-term care insurance involves careful consideration of policy features, premiums, and the financial stability of the insurer. It’s an investment in your future well-being and financial security.

Understanding Policy Features and Benefits

Long-term care insurance policies are not all the same; they come with various features and benefit structures. Understanding these is vital to choosing a policy that aligns with your needs and budget.

- Daily Benefit Amount: The maximum amount the policy will pay for care services per day.

- Benefit Period: The duration (e.g., 2 years, 5 years, lifetime) for which the policy will pay benefits.

- Elimination Period: A waiting period (e.g., 30, 60, or 90 days) during which you pay for care out-of-pocket before the policy begins to pay.

- Inflation Protection: An important feature that increases your daily benefit amount over time to keep pace with rising care costs.

Premiums for long-term care insurance are generally lower when purchased at a younger age and in good health. It’s advisable to compare policies from multiple providers and consult with a financial advisor to determine the best fit for your individual circumstances. This proactive approach can significantly impact your financial readiness for future care needs.

Alternative Funding Strategies for Long-Term Care

While long-term care insurance and government programs are significant avenues, other financial strategies can also be employed to cover potential long-term care costs. A diversified approach often provides the most robust plan, combining different methods to build a secure future. These alternatives can complement traditional insurance or serve as primary funding sources depending on individual circumstances.

Exploring these options allows for a more tailored and flexible approach to long-term care planning, addressing specific financial situations and preferences. It’s about building a resilient financial framework.

Hybrid Policies and Self-Funding Options

- Life Insurance with Long-Term Care Riders: Allows you to access a portion of your life insurance death benefit early to cover long-term care expenses. If you don’t use the long-term care benefit, your beneficiaries still receive the death benefit.

- Annuities with Long-Term Care Benefits: Provides income for life, and some annuities can be structured to provide enhanced payments if you need long-term care.

- Self-Funding/Personal Savings: For those with substantial assets, self-funding through dedicated savings accounts, investments, or leveraging home equity can be a viable strategy. This requires careful financial management and a thorough assessment of potential costs.

Each of these strategies has its own advantages and disadvantages, and the best choice depends on your financial situation, risk tolerance, and future goals. Consulting with a financial planner specializing in elder care can help you navigate these complex choices and create a personalized plan.

Proactive Planning: Steps to Take Before 2026

The best time to plan for long-term care is now, not when the need arises. Proactive planning allows you to explore all options, make informed decisions, and secure the best possible care without undue financial strain. Delaying this crucial process can limit your choices and increase stress during an already challenging time.

Beginning the planning process involves several key steps, from assessing your potential needs to consulting with professionals. This systematic approach ensures a comprehensive and effective strategy.

Key Actions for Future Healthcare Preparedness

Taking concrete steps today can significantly impact your future long-term care experience. These actions empower you to take control of your future healthcare needs and costs.

- Assess Your Needs: Consider your family health history, lifestyle, and financial situation to estimate the likelihood and potential duration of needing long-term care.

- Research Costs: Investigate the current and projected costs of long-term care services in your desired geographic area.

- Review Insurance Options: Explore private long-term care insurance, hybrid policies, and other insurance products that might offer coverage.

- Consult Financial Professionals: Work with a financial advisor specializing in long-term care planning to develop a personalized strategy that integrates with your overall financial goals.

- Understand Government Programs: Familiarize yourself with eligibility requirements for Medicare, Medicaid, and other state or federal benefits that could provide assistance.

- Legal Documents: Ensure you have essential legal documents in place, such as a durable power of attorney for healthcare and a living will, to articulate your wishes.

By taking these steps, you can build a robust plan that addresses the complexities of Long-Term Care Benefits 2026: Planning Ahead for Future Healthcare Needs and Costs. This proactive approach ensures that you and your loved ones are well-prepared for whatever the future may hold, providing security and peace of mind.

| Key Aspect | Brief Description |

|---|---|

| Understanding Care | Long-term care covers medical and non-medical services for chronic illness or disability, including home care, assisted living, and nursing homes. |

| Cost Projections | Costs are escalating due to inflation and demand, potentially reaching over $100,000 annually for nursing home care by 2026. |

| Funding Options | Options include private long-term care insurance, hybrid policies, self-funding, and government programs like Medicaid (with strict eligibility). |

| Proactive Planning | Start early by assessing needs, researching costs, consulting advisors, and understanding all available benefit programs to secure your future. |

Frequently Asked Questions About Long-Term Care Benefits 2026

Long-term care involves ongoing medical and non-medical support for individuals facing chronic illness or disability, affecting daily activities. Planning by 2026 is crucial because costs are projected to rise significantly, and early preparation ensures access to preferred care options without depleting personal assets.

No, Medicare generally does not cover long-term custodial care. It primarily covers short-term skilled nursing or home health care following a hospital stay. For extensive, ongoing personal care, Medicare provides very limited coverage, making alternative planning essential for 2026.

Key strategies include purchasing private long-term care insurance, utilizing hybrid policies (life insurance with LTC riders), self-funding through savings and investments, and exploring eligibility for government programs like Medicaid, which has strict income and asset requirements.

The ideal time to start planning for long-term care benefits is typically in your 50s or early 60s. Purchasing insurance when you are younger and healthier often results in lower premiums and easier eligibility. Proactive planning secures more options.

You can estimate costs by researching average rates for home care, assisted living, and nursing homes in your area, considering inflation, and assessing your likely health trajectory based on family history. Consulting a financial advisor can provide a more personalized projection.

Conclusion

The landscape of Long-Term Care Benefits 2026: Planning Ahead for Future Healthcare Needs and Costs is complex, but with proactive engagement, it is entirely navigable. Understanding the types of care available, the escalating costs, the role of government programs, and the various private funding strategies empowers individuals and families to make informed decisions. By taking deliberate steps today, such as assessing needs, researching options, and consulting financial professionals, you can secure not only your financial well-being but also access to the quality care you deserve in the future. Planning ahead ensures peace of mind and safeguards your legacy against unforeseen healthcare expenses.