Navigating Student Loan Repayment in 2026: New Federal Aid Changes

Advertisers

US borrowers must familiarize themselves with the upcoming federal aid program changes in 2026 to effectively navigate student loan repayment and adapt their financial strategies accordingly.

As 2026 rapidly approaches, millions of US borrowers are looking ahead to significant shifts in federal student aid programs. Understanding these impending changes is crucial for anyone with outstanding educational debt. This comprehensive guide will help you in navigating student loan repayment in 2026, ensuring you are well-prepared for what lies ahead.

Advertisers

Understanding the Evolving Landscape of Federal Student Aid

The federal student aid landscape is in a constant state of evolution, driven by economic shifts, legislative priorities, and the ongoing effort to make higher education more accessible and affordable. For US borrowers, this means a continuous need to stay informed about new policies and program adjustments that can directly impact their financial well-being. The changes slated for 2026 are particularly noteworthy, promising a mix of new opportunities and potential challenges.

Advertisers

These modifications are often designed to streamline processes, introduce new repayment flexibilities, or recalibrate existing aid structures. While the overarching goal is typically to alleviate borrower burden, the specifics can sometimes be complex and require careful interpretation. Being proactive in understanding these shifts is the first step toward effective debt management.

Key Legislative Drivers Behind the 2026 Changes

Several legislative actions and administrative reviews have paved the way for the 2026 federal student aid program changes. These often stem from a desire to address long-standing issues within the student loan system, such as high default rates or the perceived unfairness of certain repayment structures. Understanding the motivations behind these changes can provide valuable context.

- Economic Impact: Response to inflation and economic forecasts affecting borrower capacity.

- Equity Concerns: Efforts to create a more equitable system for historically underserved communities.

- Simplification Initiatives: Attempts to reduce complexity in application and repayment processes.

- Sustainability Goals: Strategies to ensure the long-term viability of federal student aid programs.

Ultimately, the evolving landscape reflects a dynamic interplay between governmental policy, economic realities, and the lived experiences of millions of student loan borrowers. Staying abreast of these developments is not just about compliance, but about optimizing your financial future.

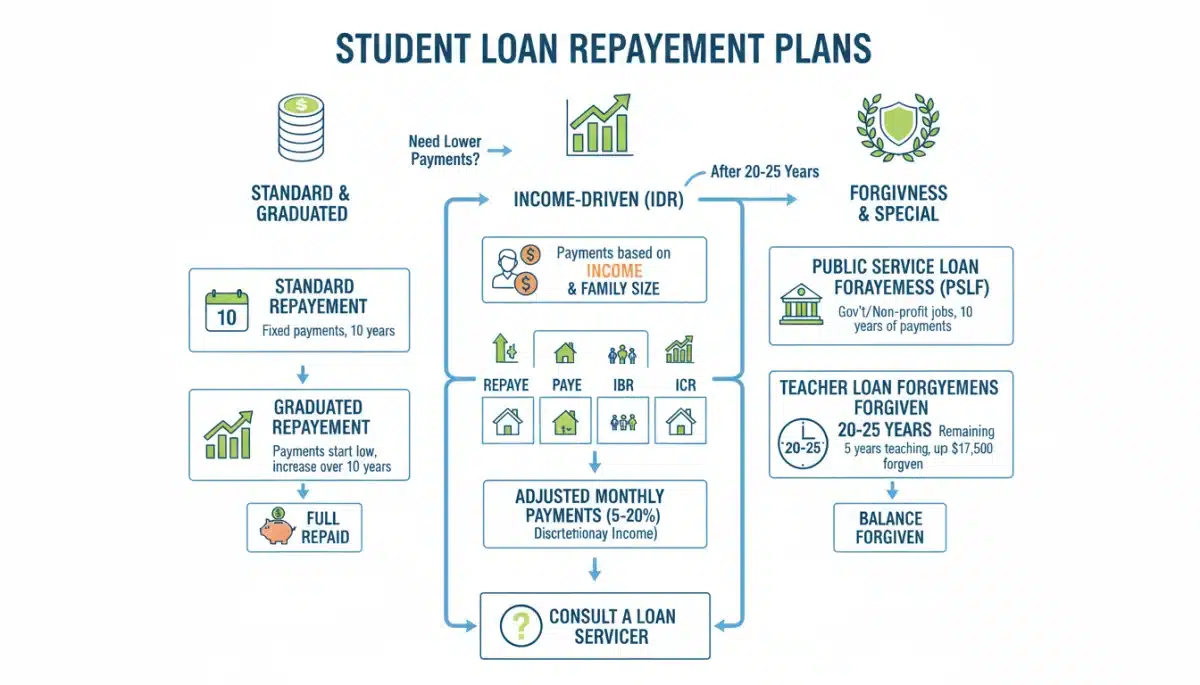

New Repayment Plans and Their Impact on Borrowers

One of the most significant aspects of the 2026 changes involves the introduction or modification of federal student loan repayment plans. These plans are the backbone of how borrowers manage their debt, determining monthly payments, interest accrual, and potential for loan forgiveness. A thorough understanding of these new options is paramount for all US borrowers.

The government continually seeks to refine these plans to better meet the diverse financial situations of borrowers. New plans might offer lower monthly payments, different interest subsidies, or revised timelines for loan forgiveness. Conversely, some existing plans may see their terms altered, necessitating a review of your current repayment strategy.

Exploring the SAVE Plan Enhancements

The Saving on a Valuable Education (SAVE) Plan, for instance, is expected to see further enhancements in 2026, building upon its initial rollout. These enhancements aim to provide even more relief to borrowers, particularly those with lower incomes or larger loan balances. Key features could include further reductions in discretionary income calculations or expanded eligibility.

- Lower Monthly Payments: Potential for payments to be calculated on an even smaller percentage of discretionary income.

- Interest Subsidies: Continued or enhanced interest benefits to prevent balances from growing due to unpaid interest.

- Expanded Eligibility: Broader criteria for who can qualify for the most favorable terms of the plan.

Borrowers currently enrolled in other income-driven repayment (IDR) plans, such as PAYE or IBR, should carefully evaluate whether switching to an enhanced SAVE Plan would be beneficial. The decision hinges on individual financial circumstances, loan types, and long-term financial goals. Consulting with a financial advisor specializing in student loans can provide tailored guidance.

Eligibility Requirements and Application Processes

With any changes to federal aid programs come updated eligibility requirements and potentially revised application processes. For US borrowers, understanding who qualifies for new benefits and how to apply is critical to taking advantage of the favorable terms available in 2026. These requirements can vary significantly depending on the specific program or repayment plan.

Eligibility often hinges on factors such as loan type (federal vs. private), income level, family size, and employment status. The application process, while generally streamlined, may require new documentation or adherence to different deadlines. Proactive preparation can prevent delays or missed opportunities.

Navigating the Federal Student Aid Website

The official Federal Student Aid (FSA) website remains the primary resource for all information regarding eligibility and application. Borrowers should regularly check this site for updates, as program details and forms can be modified without extensive prior notice. The website offers tools and resources designed to help you understand your options.

- Account Access: Ensure your FSA ID is active and you can log in to view your loan details.

- Documentation Checklist: Gather necessary financial documents, such as tax returns and pay stubs, in advance.

- Online Application Portal: Familiarize yourself with the online application system for new repayment plans or forgiveness programs.

It is important to remember that eligibility for one program does not automatically guarantee eligibility for another. Each program has its own specific criteria, and borrowers must review them carefully to determine the best path forward. Timely and accurate submission of all required information is key to a smooth application process.

Strategies for Optimizing Your Repayment Plan

Beyond simply understanding the changes, US borrowers need concrete strategies to optimize their student loan repayment in 2026. This involves more than just selecting a plan; it requires a holistic approach to financial management that considers your budget, career trajectory, and long-term financial aspirations. Optimization means finding the most efficient and least burdensome path to becoming debt-free.

The goal is to minimize interest paid, maximize potential for loan forgiveness, and ensure monthly payments are sustainable. This might involve a combination of strategies, from consolidating loans to exploring public service loan forgiveness (PSLF) if applicable. Each borrower’s situation is unique, necessitating a personalized approach.

Considering Loan Consolidation and Refinancing

Loan consolidation, particularly federal direct loan consolidation, can simplify your repayment by combining multiple federal loans into a single new loan with one monthly payment. This can also potentially open avenues to new repayment plans or loan forgiveness programs. Refinancing, usually with a private lender, involves taking out a new loan to pay off existing federal or private loans, often at a lower interest rate.

- Federal Consolidation: Simplifies payments, potentially lowers monthly payment, and can qualify for IDR plans or PSLF.

- Private Refinancing: Can offer lower interest rates for borrowers with excellent credit, but forfeits federal loan benefits.

- Strategic Timing: Evaluate market interest rates and your financial stability before deciding on either option.

Carefully weigh the pros and cons of both consolidation and refinancing. While a lower interest rate from refinancing can be attractive, losing access to federal benefits like IDR plans, deferment, forbearance, and loan forgiveness programs can be a significant drawback for many. Federal consolidation, on the other hand, preserves these benefits while streamlining your loans.

The Role of Public Service Loan Forgiveness (PSLF) and Other Forgiveness Programs

For US borrowers working in qualifying public service jobs, the Public Service Loan Forgiveness (PSLF) program remains a vital pathway to debt relief. The 2026 changes could bring further clarifications or adjustments to this program, making it crucial for eligible individuals to stay informed. Beyond PSLF, other forgiveness or discharge programs may also be available under specific circumstances.

PSLF allows the remaining balance on Direct Loans to be forgiven after 120 qualifying monthly payments are made under a qualifying repayment plan while working full-time for a qualifying employer. Ensuring you meet all criteria is essential, as even minor missteps can jeopardize your eligibility.

Key Considerations for PSLF Eligibility

The requirements for PSLF are stringent and require meticulous record-keeping. The type of loans, repayment plan, employer, and number of payments all play a critical role. The Department of Education often provides updates and tools to help borrowers track their progress and confirm eligibility.

- Loan Type: Only Direct Loans qualify; other federal loans may need to be consolidated.

- Repayment Plan: Must be an income-driven repayment plan or the 10-year standard repayment plan.

- Qualifying Employment: Work for a government organization (federal, state, local, tribal) or a not-for-profit organization.

- Payment Tracking: Submit the PSLF Employment Certification Form annually or whenever you change employers.

Beyond PSLF, be aware of other potential forgiveness or discharge options, such as teacher loan forgiveness, total and permanent disability discharge, or discharge due to school closure. Each program has specific criteria, and borrowers should research them thoroughly to see if they qualify. The 2026 landscape might introduce new avenues for relief, so staying updated is paramount.

Preparing for Future Financial Well-being

Effective student loan repayment in 2026 is not just about managing current debt; it’s about setting yourself up for future financial well-being. The strategies you employ now will have lasting impacts on your credit score, ability to save, and overall financial stability. Proactive planning and continuous monitoring of your loan status are essential components of this preparation.

This includes building an emergency fund, making informed decisions about additional education or career changes, and regularly reviewing your budget. The goal is to integrate your student loan strategy into your broader financial plan, ensuring it supports rather than hinders your long-term goals.

Utilizing Financial Counseling and Resources

Many resources are available to help US borrowers navigate the complexities of student loan repayment. The Department of Education offers free financial counseling, and non-profit organizations specialize in providing guidance on debt management. These resources can offer personalized advice and help you understand the nuances of the 2026 changes.

- Official Department of Education Resources: Utilize their website, hotline, and financial aid counselors.

- Accredited Non-Profit Credit Counselors: Seek advice from organizations specializing in student loan debt.

- Financial Planning Professionals: Consider consulting a certified financial planner for comprehensive financial advice.

Remember, your financial situation is dynamic. What works today might need adjustment tomorrow. Regularly reassessing your repayment strategy, staying informed about policy changes, and leveraging available resources will empower you to manage your student loans effectively and build a strong financial foundation for the future.

| Key Aspect | Brief Description |

|---|---|

| New Repayment Plans | Federal aid programs in 2026 introduce new or enhanced repayment options, potentially offering lower monthly payments and revised forgiveness timelines. |

| Eligibility Updates | Borrowers must review updated criteria for new programs, often based on income, loan type, and employment, to qualify for benefits. |

| SAVE Plan Enhancements | The SAVE Plan is expected to offer further borrower relief through reduced discretionary income calculations and enhanced interest subsidies. |

| PSLF & Forgiveness | Public Service Loan Forgiveness continues to be a key option, with potential clarifications; other forgiveness programs remain vital. |

Frequently Asked Questions About 2026 Student Loan Changes

The biggest changes expected in 2026 include enhancements to income-driven repayment plans like SAVE, potentially leading to lower monthly payments and improved interest subsidies. There may also be updated eligibility criteria for various aid programs and refined pathways to loan forgiveness for US borrowers.

The SAVE Plan is anticipated to offer further borrower-friendly adjustments in 2026. These could involve calculating payments based on an even smaller percentage of discretionary income and providing more robust interest subsidies to prevent loan balances from increasing due to unpaid interest.

Consolidating federal student loans before 2026 could be beneficial if it allows you to qualify for certain repayment plans or forgiveness programs that you wouldn’t otherwise access. However, it’s crucial to evaluate how consolidation impacts your interest rate and any potential loss of borrower benefits. Consult a financial advisor for personalized guidance.

While PSLF’s core structure is expected to remain, 2026 might bring clarifications or minor adjustments to its eligibility requirements or payment tracking. Borrowers pursuing PSLF should continue to certify their employment annually and stay informed through the official Federal Student Aid website for any updates.

The most reliable and up-to-date information regarding federal aid program changes will always be available on the official Federal Student Aid (FSA) website, studentaid.gov. It is recommended to regularly check this site for announcements, guides, and tools to help you navigate your student loan repayment.

Conclusion

The upcoming federal aid program changes in 2026 represent a critical juncture for millions of US borrowers. Understanding these modifications, from new repayment plan enhancements like those for the SAVE Plan to updated eligibility criteria for various forgiveness programs, is not merely advisable but essential. By proactively engaging with these developments, leveraging available resources, and strategically planning your repayment, you can confidently navigate the evolving landscape of student loan debt and secure a more stable financial future. Staying informed and adaptable will be your greatest assets in the years to come.