COBRA Benefits 2026: Continuing Health Coverage After Job Loss

Advertisers

COBRA benefits in 2026 provide eligible individuals and their families with the option to continue their employer-sponsored health coverage temporarily after certain qualifying events like job loss.

Advertisers

Navigating healthcare coverage after a job loss can be a daunting experience, filled with uncertainty and complex decisions. For many in the United States, the Consolidated Omnibus Budget Reconciliation Act (COBRA) offers a vital bridge, allowing continued access to employer-sponsored health plans. Understanding COBRA benefits in 2026 is crucial for anyone facing this transition, ensuring that you and your family maintain essential health coverage without interruption. This comprehensive guide will demystify COBRA, outlining its eligibility requirements, costs, duration, and alternatives, empowering you to make informed choices during a challenging time.

Advertisers

understanding COBRA: what it is and who it covers

COBRA is a federal law that provides workers and their families who lose their health benefits the right to choose to continue group health benefits provided by their group health plan for limited periods of time under certain circumstances. These circumstances include voluntary or involuntary job loss, reduction in hours worked, transition between jobs, death, divorce, and other life events. In 2026, the fundamental principles of COBRA remain consistent, offering a safety net for individuals and families suddenly without employer-provided health insurance.

The law was enacted to protect employees and their families from the immediate loss of health coverage, which could lead to significant financial strain during periods of unemployment or other qualifying events. It applies to group health plans maintained by employers with 20 or more employees on more than 50% of their typical business days in the previous calendar year. This threshold is important, as smaller employers are generally exempt from COBRA requirements, though state-specific mini-COBRA laws might apply.

eligibility for COBRA coverage

- Qualifying Event: This is a specific event that causes an individual to lose their group health coverage, such as job termination (except for gross misconduct), reduction in hours, death of the covered employee, divorce or legal separation, or a child losing dependency status.

- Qualified Beneficiary: This includes the covered employee, their spouse, and dependent children who were covered under the group health plan on the day before the qualifying event.

- Employer Size: The employer must have had 20 or more employees during the preceding calendar year.

It is important to note that COBRA only extends the existing group health coverage; it does not introduce new benefits or change the plan design. Therefore, if your employer’s plan changes, your COBRA coverage will also reflect those changes. Understanding these foundational aspects is the first step in determining if COBRA is the right path for your health coverage needs in 2026.

the cost of COBRA benefits in 2026

One of the most significant considerations when electing COBRA is its cost. Unlike employer-sponsored coverage where the employer typically subsidizes a large portion of the premiums, under COBRA, you are generally responsible for the entire premium cost, plus an administrative fee. This can make COBRA significantly more expensive than what you were paying as an active employee.

The cost of COBRA coverage is determined by the actual cost of the group health plan. This includes both the portion the employee previously paid and the portion the employer previously contributed. Additionally, the plan can charge a 2% administrative fee, bringing the total cost up to 102% of the premium. This means that a plan that cost $500 per month with an employer contribution might now cost you $510 per month under COBRA.

factors influencing COBRA premiums

- Plan Type: The type of health plan (HMO, PPO, HDHP) and its associated benefits will directly impact the premium. More comprehensive plans naturally come with higher costs.

- Coverage Level: Whether you’re covering just yourself, yourself and a spouse, or your entire family will also affect the total premium.

- Administrative Fees: The 2% administrative fee is standard across most COBRA plans, adding a small but consistent amount to the overall cost.

It’s crucial to obtain an accurate quote for your specific COBRA premium from your former employer or plan administrator. This will allow you to budget effectively and compare it against other available health coverage options. While the cost can be high, the benefit of maintaining continuity of care and avoiding gaps in coverage often outweighs the expense for many individuals, particularly those with ongoing medical conditions or specific doctor preferences.

duration and extension options for COBRA coverage

COBRA coverage is not indefinite; it is designed to be a temporary extension of health benefits. The standard maximum period for COBRA coverage is 18 months, typically for qualifying events such as termination of employment or reduction in hours. However, certain circumstances can allow for extensions beyond this initial period, providing additional peace of mind during extended transitions.

For other qualifying events, such as the death of the covered employee, divorce, or a child losing dependency status, spouses and dependent children may be eligible for up to 36 months of COBRA coverage. It’s vital to understand these different durations as they directly impact your long-term healthcare planning.

key extension scenarios for 2026

- Second Qualifying Event: If a second qualifying event (like divorce or a child losing dependency) occurs during the initial 18-month COBRA period, the maximum coverage period can be extended to 36 months from the date of the original qualifying event.

- Disability Extension: Qualified beneficiaries who are determined by the Social Security Administration (SSA) to be disabled within the first 60 days of COBRA coverage may be eligible for an additional 11 months of coverage, extending the total to 29 months. This requires notification to the plan administrator.

It is imperative to notify your plan administrator promptly of any such events that might qualify you for an extension. Missing deadlines can result in the loss of your right to extended coverage. Keeping accurate records and communicating proactively are key to maximizing your COBRA benefits. The temporary nature of COBRA underscores the importance of exploring alternative coverage well before your COBRA period expires.

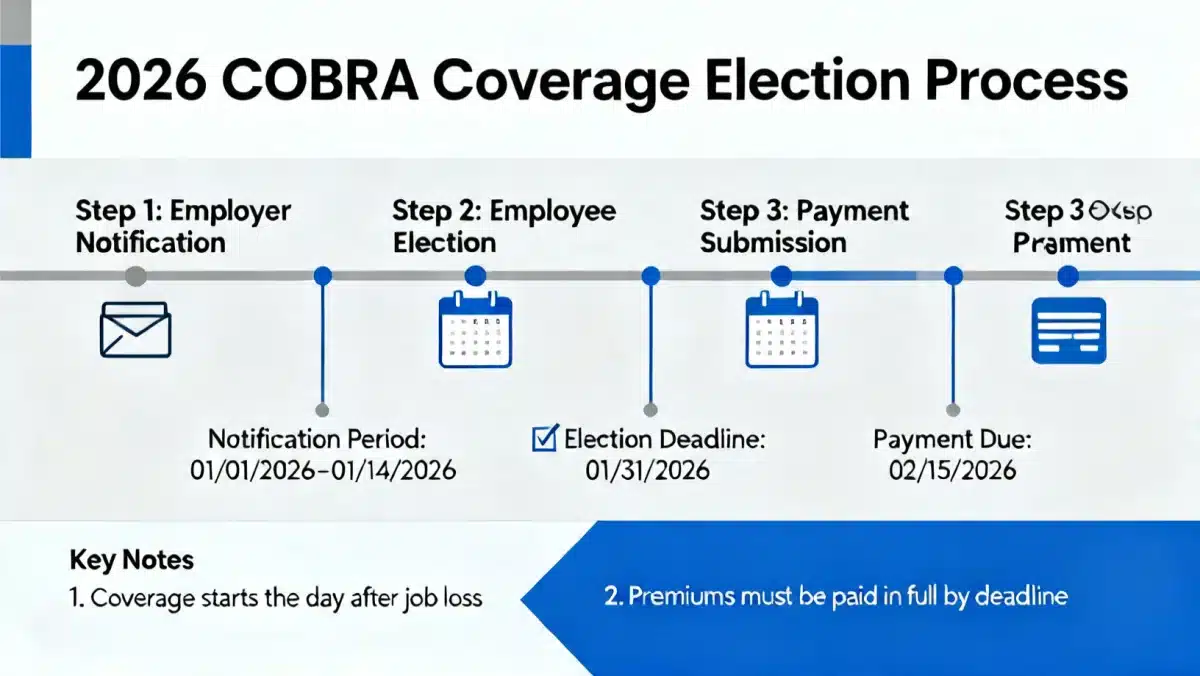

electing COBRA: steps and deadlines in 2026

The process of electing COBRA coverage involves several steps and strict deadlines that must be adhered to. Missing these deadlines can lead to the forfeiture of your right to COBRA, leaving you without health insurance. Understanding the timeline and required actions is crucial for anyone considering this option after a qualifying event.

Generally, once a qualifying event occurs, your employer has 30 days to notify the plan administrator. The plan administrator then has 14 days to provide you with an election notice, which details your rights and options under COBRA. Upon receiving this notice, you typically have 60 days to decide whether to elect COBRA coverage. This 60-day election period begins on the date the election notice is provided or the date your group health coverage would otherwise end, whichever is later.

critical deadlines to remember

- Employer Notification: Your employer must notify the plan administrator within 30 days of your qualifying event.

- Plan Administrator Notification: The plan administrator must send you an election notice within 14 days of receiving notification from your employer.

- Election Period: You have 60 days from the date of the election notice (or loss of coverage, whichever is later) to elect COBRA.

- First Premium Payment: Once you elect COBRA, you have 45 days from the date of election to make your first premium payment. Subsequent payments are typically due on a monthly basis, with a 30-day grace period.

It’s important to carefully review all documents provided by your plan administrator and to keep copies for your records. If you do not receive an election notice within a reasonable timeframe after your qualifying event, contact your former employer or the plan administrator immediately. Proactive engagement ensures you do not miss out on your opportunity for COBRA coverage.

alternatives to COBRA: exploring other health coverage options

While COBRA offers a valuable continuation of coverage, its high cost can be a deterrent for many. Fortunately, several alternatives exist that might be more affordable or better suited to your specific needs in 2026. Exploring these options in parallel with considering COBRA can help you find the best solution for your health insurance requirements after job loss.

One of the primary alternatives is the Health Insurance Marketplace (also known as the exchange) established under the Affordable Care Act (ACA). Losing job-based health coverage is considered a qualifying life event that triggers a Special Enrollment Period (SEP), allowing you to enroll in a new plan through the Marketplace outside of the annual open enrollment period. Plans on the Marketplace may offer premium tax credits and cost-sharing reductions based on your income, potentially making them significantly more affordable than COBRA.

other viable health insurance options

- Spouse’s Plan: If your spouse has employer-sponsored health coverage, you may be able to enroll in their plan during a Special Enrollment Period triggered by your job loss. This is often a more cost-effective solution than COBRA.

- Medicaid: If your income falls below a certain threshold, you might be eligible for Medicaid, a joint federal and state program that provides free or low-cost health coverage to low-income individuals and families. Eligibility rules vary by state.

- Short-Term Health Insurance: These plans offer temporary coverage and are generally much cheaper than COBRA or Marketplace plans. However, they do not have to cover essential health benefits, may not cover pre-existing conditions, and are not regulated by the ACA. They are typically best for those who expect a very short gap in coverage.

Carefully compare the benefits, costs, and provider networks of each option before making a decision. The Marketplace is often a strong contender due to potential subsidies and comprehensive coverage. Consulting with a healthcare navigator or insurance broker can also provide personalized guidance based on your financial situation and health needs.

navigating COBRA and the ACA marketplace in 2026

The interplay between COBRA and the Affordable Care Act (ACA) Marketplace can sometimes be confusing, but understanding their relationship is key to making the most informed decision about your health coverage. While COBRA provides a continuation of your previous employer plan, the Marketplace offers new, often subsidized, plans.

When you lose job-based coverage, you gain a Special Enrollment Period (SEP) to enroll in a Marketplace plan. This SEP typically lasts 60 days from the date you lose your coverage. You can choose to elect COBRA, or you can opt for a Marketplace plan. It’s important to weigh the pros and cons of each. COBRA provides continuity with your existing doctors and benefits, but often at a higher cost. Marketplace plans might be more affordable, especially with subsidies, but could require you to change doctors or adjust to a new network.

key considerations for choice

- Cost Comparison: Calculate the exact cost of COBRA versus the subsidized premium of a Marketplace plan. Don’t forget to factor in deductibles, copayments, and out-of-pocket maximums.

- Provider Network: Check if your preferred doctors and specialists are in-network with a potential Marketplace plan. If continuity of care is paramount, COBRA might be preferable despite the cost.

- Prescription Coverage: Compare prescription drug formularies to ensure your medications are covered and at an affordable tier under both options.

You are allowed to elect COBRA and then later switch to a Marketplace plan, but there are nuances. If you elect COBRA, you generally cannot drop it mid-term to get a new SEP for the Marketplace unless your COBRA coverage ends or you experience another qualifying life event. However, you can always switch to a Marketplace plan during the annual Open Enrollment Period, regardless of your COBRA status. This flexibility, combined with careful financial and medical assessment, will guide your decision in 2026.

important updates and considerations for 2026

As we move into 2026, the landscape of healthcare benefits, including COBRA, continues to evolve. While the core tenets of COBRA remain stable, staying informed about any potential legislative changes, administrative adjustments, or economic factors that might influence health insurance costs and accessibility is always wise. Although major overhauls of COBRA are not typically frequent, minor adjustments or interpretations can occur.

One area to consistently monitor is the inflation rate in healthcare costs. Premiums for all types of health insurance, including COBRA, are influenced by general medical inflation. As healthcare costs rise, so too will the premiums for COBRA coverage. Therefore, even if the legal framework of COBRA remains unchanged, the financial burden might incrementally increase year over year. This makes the comparison with Marketplace plans, which can offset some of these increases with subsidies, even more critical.

staying informed and prepared

- Review Employer Communications: Pay close attention to any communications from your former employer or plan administrator regarding your health benefits. These often contain crucial information about COBRA election periods and any plan changes.

- Consult Official Sources: For the most accurate and up-to-date information on COBRA and healthcare laws, refer to official government websites such as the Department of Labor (DOL) and the Centers for Medicare & Medicaid Services (CMS).

- Seek Professional Advice: If your situation is complex, consider consulting with a benefits specialist, financial advisor, or an attorney specializing in healthcare law. They can provide tailored advice based on your individual circumstances.

Being proactive and well-informed is your best defense against unexpected healthcare costs or coverage gaps. Understanding these evolving considerations will help you better plan for your health coverage needs, ensuring that you maintain access to necessary medical care throughout 2026 and beyond, regardless of your employment status.

| Key Aspect | Brief Description |

|---|---|

| Eligibility | Applies to employers with 20+ employees; covers job loss, divorce, etc., for employee, spouse, dependents. |

| Cost | 100% of premium + 2% administrative fee; often significantly higher than active employee rates. |

| Duration | Generally 18 months for job loss; up to 36 months for other events or with extensions (e.g., disability). |

| Alternatives | ACA Marketplace (with potential subsidies), spouse’s plan, Medicaid, or short-term insurance. |

frequently asked questions about COBRA in 2026

The primary purpose of COBRA is to provide a temporary continuation of group health coverage for individuals and their families who would otherwise lose their benefits due to certain qualifying events, such as job loss. This bridges the gap, preventing immediate loss of vital health insurance.

COBRA can be expensive because you are responsible for the full premium, including the portion your employer previously paid, plus a 2% administrative fee. This means the cost can be up to 102% of the total premium, often significantly higher than what you paid as an active employee.

Yes, you can. Losing job-based coverage triggers a Special Enrollment Period for the ACA Marketplace. While you can elect COBRA, you can later switch to a Marketplace plan during its annual Open Enrollment Period or if another qualifying life event occurs, like COBRA coverage ending.

After your employer notifies the plan administrator of a qualifying event, you’ll receive an election notice. From the date of this notice (or loss of coverage, whichever is later), you typically have 60 days to elect COBRA. Missing this deadline means forfeiting your right to coverage.

Yes. The standard 18-month period can be extended to 36 months for a second qualifying event, or up to 29 months if a qualified beneficiary is determined to be disabled by the SSA within the first 60 days of COBRA coverage. Proper notification is essential for these extensions.

conclusion

Navigating the complexities of health coverage after job loss in 2026 demands careful consideration and proactive planning. COBRA benefits in 2026 offer a critical, albeit often costly, option to maintain continuity of care, allowing individuals and families to avoid gaps in their health insurance. However, it is equally important to explore alternatives such as the ACA Marketplace, spouse’s plans, or Medicaid, which might provide more affordable or suitable coverage based on individual circumstances. By understanding eligibility, costs, durations, and election processes, you can make informed decisions that safeguard your health and financial well-being during periods of transition. Remaining vigilant about deadlines and seeking professional advice when needed will ensure you secure the best possible health insurance solution for your needs.